More Fun with the Principal-Agent Model

Christopher Makler

Stanford University Department of Economics

Econ 51: Lecture 18

Please fill out the course evaluations.

To the extent that this has been a good course, it's due in large part to the feedback I've gotten from students like you over the years.

Help me make it even better for the next group!

A reminder...

If people have hidden information,

(e.g. the quality of a used car for sale)

what mechanism can a designer establish

to get them to reveal that information?

If people can take hidden actions,

what mechanism can a designer establish

to get them to choose the action the designer wants them to take?

ADVERSE SELECTION

MORAL HAZARD

Principal: Someone who needs someone else to do something

Agent: The person who needs to do the thing

CEO / sales rep

Professor / student

Landowner / farmer

The principal's payoff depends on the actions of the agent

Can they incentivize the agent to do what they want?

Principal-Agent Model

The agent can choose whether to exert effort (E), shirk/not exert effort (N), or reject the contract altogether (R)

Their effort choice is unobservable to the principal.

Model 1 (Last time): Discrete choice of effort

The principal's problem is to choose a wage structure that maximizes their own expected payoff

If they want to get the agent to choose E, they need to make choosing E the best choice:

Incentive compatibility constraint: E must be at least as good as N

Participation constraint: Accepting the contract (and exerting effort E)

must be at least as good as rejecting it (R).

The agent chooses how much effort to exert.

Their effort choice is unobservable to the principal.

Model 2: Continuous choice of effort

The principal's problem is to choose a wage structure that maximizes their own expected payoff

Their problem is to choose the wage contract that incentivizes the agent to choose the profit-maximizing E*

Working on Commission

A publisher (principal) wants to hire an salesperson (agent) to go door-to-door selling books.

Each book is sold for $80.

📕

👩🏻🏫

👨🏻💼

Publisher (principal)

Salesperson (agent)

The agent gets fraction \(\theta\) of the $80 as a commission.

The principal gets fraction \(1 - \theta\) of the $80

80(1-\theta)

80\theta

💵

A publisher (principal) wants to hire an salesperson (agent) to go door-to-door selling books.

Each book is sold for $80.

📕

👩🏻🏫

👨🏻💼

Publisher (principal)

Salesperson (agent)

The agent gets fraction \(\theta\) of the $80 as a commission.

The principal gets fraction \(1 - \theta\) of the $80

80(1-\theta)

80\theta

💵

The probability that a sale is made is a function of the agent's effort: Prob { success | e } = \(\sqrt{e}\)

u_P(e) = 80(1-\theta)\sqrt{e}

Each unit of effort costs the agent 40: that is, \(c(e) = 40e\)

u_A(e) = 80\theta\sqrt{e} - 40e

👩🏻🏫

👨🏻💼

Publisher (principal)

Salesperson (agent)

u_P(e) = 80(1-\theta)\sqrt{e}

u_A(e) = 80\theta\sqrt{e} - 40e

What is the efficient amount of effort, \(e^*\)?

(We can define efficiency here as

maximizing the sum of the payoffs.)

pollev.com/chrismakler

👩🏻🏫

👨🏻💼

Publisher (principal)

Salesperson (agent)

u_P(e) = 80(1-\theta)\sqrt{e}

u_A(e) = 80\theta\sqrt{e} - 40e

+

u_P(e)

80(1-\theta)\sqrt{e}

u_A(e)

80\theta\sqrt{e} - 40e

+

=

= 80\sqrt e - 40e

W(e)=

W'(e)= {40 \over \sqrt{e}} - 40 = 0

\Rightarrow e^* = 1

W(1) = 80 - 40 = 40

Maximum possible welfare:

To maximize, take the derivative and set equal to zero:

👩🏻🏫

👨🏻💼

Publisher (principal)

Salesperson (agent)

u_P(e) = 80(1-\theta)\sqrt{e}

u_A(e) = 80\theta\sqrt{e} - 40e

What level of effort will the salesperson choose, given the commission \(\theta\) they receive?

u_A^\prime(e) = {40\theta \over \sqrt{e}} - 40 = 0

e^*(\theta)=

\theta^2

u_P(\theta) = 80(1-\theta)\sqrt{e^*(\theta)}

= 80(1-\theta)\theta

= 80(\theta - \theta^2)

u_P^\prime(\theta) = 80(1-2\theta) = 0

\Rightarrow \theta^* = \tfrac{1}{2}

Given this response to \(\theta\), what commission \(\theta\) maximizes the principal's payoff?

👩🏻🏫

👨🏻💼

Publisher (principal)

Salesperson (agent)

u_P(e) = 80(1-\theta)\sqrt{e}

u_A(e) = 80\theta\sqrt{e} - 40e

e^*(\theta)=

\theta^2

\theta^* = \tfrac{1}{2}

=\tfrac{1}{4}

u_P = 80(1-\tfrac{1}{2})\sqrt{\tfrac{1}{4}}

What are the payoffs to each player?

= 20

u_A = 80 \times \tfrac{1}{2} \times \sqrt{\tfrac{1}{4}} - 40 \times \tfrac{1}{4}

= 10

Note: the sum of these is 30, which is less than the 40

which would be generated if the ssalesperson exerted full effort \( (e = 1) \)

The principal is an insurance company; the agent is someone they insure.

The agent's "effort choice" is how safely or riskily to behave

Model 3: Moral hazard and insurance deductibles

If the insurance company fully insures the agent, there's no incentive to behave in a safe manner.

Their problem is to choose the an insurance contract which offers some insurance (both of them are better off) but not so much that the agent behaves recklessly.

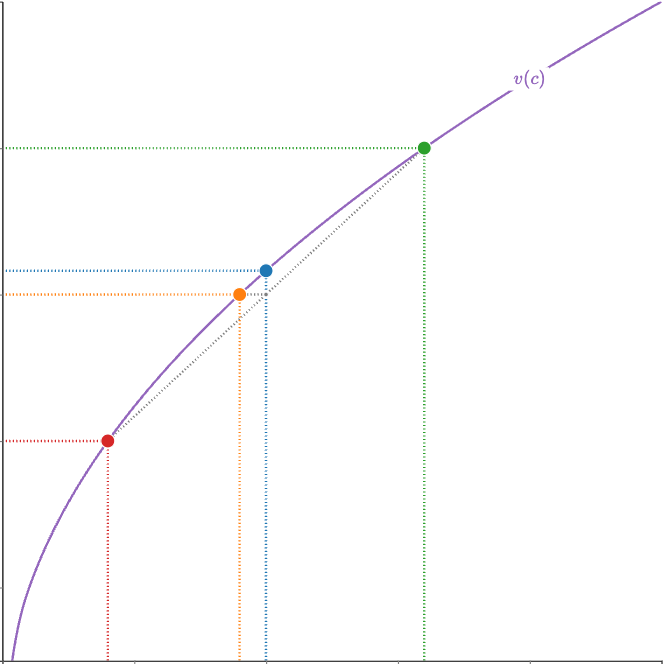

Suppose you face a lottery:

c_1 = 16

c_2 = 64

Each occurs with equal probability.

v(c) = \sqrt{c}

16

64

Utility from consumption is given by

v(c_1) = \sqrt{16}=4

\mathbb{E}[c] = \tfrac{1}{2} \times 16 + \tfrac{1}{2} \times 64 = 40

40

v(c_2) = \sqrt{64}=8

4

8

6

Consumption (dollars)

Utility (utils)

\mathbb{E}[v] = \tfrac{1}{2} \times 4 + \tfrac{1}{2} \times 8 = 6

Certainty equivalent of this lottery:

v(CE) = 6

\Rightarrow CE = 36

36

Suppose you face a lottery:

c_1 = 16

c_2 = 64

Each occurs with equal probability.

16

64

\mathbb{E}[\text{loss}] = \tfrac{1}{2} \times 48 = 24

40

4

8

6

Consumption (dollars)

Utility (utils)

Another way of thinking about this...

you currently have $64 and face a 50% chance of losing $48.

36

\mathbb{E}[c] = \tfrac{1}{2} \times 16 + \tfrac{1}{2} \times 64 = 40

\mathbb{E}[\text{loss}] = 24

WTP = 28

\text{Certainty Equivalent} = 36

- 36 = 28

How much would you be willing to pay to avoid the risk altogether?

64

16

64

\mathbb{E}[\text{loss}] = \tfrac{1}{2} \times 48 = 24

40

4

8

6

Consumption (dollars)

Utility (utils)

Another way of thinking about this...

you currently have $64 and face a 50% chance of losing $48.

36

\mathbb{E}[\text{loss}] = 24

WTP = 28

- 36 = 28

How much would you be willing to pay to avoid the risk altogether?

64

We say your risk premium is the amount you'd be willing to pay

above and beyond your expected loss,

in order to face zero risk.

In this case, that's $4.

Risk premium

But what happens if

you do fully insure?

- You pay the $28

- If the risk of loss remains 50%, the insurance company makes $4 in expectation

- But what happens if you now behave more riskily?

The agent has $64 and faces a potential loss of $48.

Probability of loss: \(\pi = 1- e\), where \(e\) is the amount of effort spent being safe

Cost of effort: \(c(e) = 4e^2\)

u(e) = \pi(e)\sqrt{16} + (1-\pi(e))\sqrt{64}-c(e)

Case 1: No Insurance

= 4 + 4e - 4e^2

u'(e) = 4 - 8e = 0

\Rightarrow e^* = \tfrac{1}{2}

u(e^*) = 4 - 4 \times \tfrac{1}{2} - 4 \times (\tfrac{1}{2})^2 = 5

The agent has $64 and faces a potential loss of $48.

Probability of loss: \(\pi = 1- e\), where \(e\) is the amount of effort spent being safe

Cost of effort: \(c(e) = 4e^2\)

u(e) = \sqrt{64 - p} - 4e^2

Case 2: Full insurance for some premium \(p\)

u'(e) = -8e

\Rightarrow e^* = 0

If you're fully insured, there's no benefit to exerting any effort to stay safe. The agent will set \(e = 0\), the probability of loss will be 1, and the insurance company would have to charge \(p = 48\) to cover the loss.

p = 48, e = 0 \Rightarrow u = \sqrt{16} = 4

The agent has $64 and faces a potential loss of $48.

Probability of loss: \(\pi = 1- e\), where \(e\) is the amount of effort spent being safe

Cost of effort: \(c(e) = 4e^2\)

u(e) = \pi(e)\sqrt{64 - p - d} + (1-\pi(e))\sqrt{64 - p} - 4e^2

Case 2: Partial insurance: premium \(p\), deductible \(d\)

If the loss occurs, you have to pay the deductible in addition to the premium

If no loss occurs, you only have to pay the premium

Example: \(p = 8\), \(d = 36\): if the loss occurs, \(c_1 = 64 - 8 - 36 = 20\); if no loss, \(c_2 = 64 - 8 = 56\):

u(e) = e\sqrt{20} + (1-e)\sqrt{56} - 4e^2

u(e) = \pi(e)\sqrt{64 - p - d} + (1-\pi(e))\sqrt{64 - p} - 4e^2

Case 2: Partial insurance: premium \(p\), deductible \(d\)

If the loss occurs, you have to pay the deductible in addition to the premium

If no loss occurs, you only have to pay the premium

Example: \(p = 8\), \(d = 36\): if the loss occurs, \(c_1 = 64 - 8 - 36 = 20\); if no loss, \(c_2 = 64 - 8 = 56\):

u(e) = (1-e)\sqrt{20} + e\sqrt{56} - 4e^2

u'(e) = -\sqrt{20} + \sqrt{56} - 8e = 0

e^* = {1 \over 8}\left(\sqrt{56} - \sqrt{20}\right) \approx 0.3764

u_A \approx 5.0388

Case 2: Partial insurance: premium \(p\), deductible \(d\)

Example: \(p = 8\), \(d = 36\): if the loss occurs, \(c_1 = 64 - 8 - 36 = 20\); if no loss, \(c_2 = 64 - 8 = 56\):

u(e) = (1-e)\sqrt{20} + e\sqrt{56} - 4e^2

u'(e) = -\sqrt{20} + \sqrt{56} - 8e = 0

e^* = {1 \over 8}\left(\sqrt{56} - \sqrt{20}\right) \approx 0.3764

u_A \approx 5.0388

What about the insurance company? They get 8 no matter what, and with probability \(1 - e \approx 0.6236\) they have to pay 12; so this is an expected profit of

u_P = 8 - 12(1-e)

\approx 8 - 0.6236 \times 12 = 0.5168

The agent has $64 and faces a potential loss of $48.

Probability of loss: \(\pi = 1- e\), where \(e\) is the amount of effort spent being safe

Cost of effort: \(c(e) = 4e^2\)

Case 2: Full insurance

e = 0

u_A = 4

e = \tfrac{1}{2}

u_A = 5

Case 1: No insurance

e \approx 0.3764

u_A \approx 5.0388

Case 3: Deductible

(no payoff to

insurance company)

u_P = 0

u_P \approx 0.5168

Key Takeaways

- Principals and agents are useful to each other: both can do better together than they could separately

- In many situations, complete contracts are not possible.

- Incomplete contracts (e.g. wages with bonus features, insurance policies with deductibles) can provide second-best options.

- The basic model is a little like Stackelberg: the first mover sets the terms, and the second mover observes that and makes their choice. The principal solves for the optimal contract using backwards induction, anticipating how the agent will respond to incentives.

Next time: Second-Degree Price Discrimination

- Creating a product line to encourage customers to "sort" themselves by their willingness to pay for quality

- Concept of "optimal ens**ttification"

Econ 51 | 18 | More Fun with the Principal-Agent Model

By Chris Makler

Econ 51 | 18 | More Fun with the Principal-Agent Model

How to design a mechanism to get someone to behave a certain way, or to reveal their true preferences