Book 2. Credit Risk

FRM Part 2

CR 22. Structured Credit Risk

Presented by: Sudhanshu

Module 1. Structured Products

Module 2. Securitization

Module 3. Simulation, Probability of Default and Default Correlation, Default Sensitivities and Structured Products

Module 1. Structured Products

Topic 1. Types of Structured Products

Topic 2. Capital Structure in Securitization

Topic 3. Waterfall Structure

Topic 1. Types of Structured Products

-

Securitization: Pooling of credit-sensitive assets and creation of new securities (structured products/portfolio credit products) whose cash flows are based on underlying loans or credit claims, with risk-return characteristics varying dramatically from original assets

-

Structured Products: New securities created through the securitization process. Each structured product has its own unique risk and return characteristics, which can differ significantly from the underlying assets.

-

Covered Bonds:

-

Structure: On-balance sheet securitizations where a mortgage pool is separated into a covered pool on the originator's balance sheet

- Investors have higher priority than general creditors in case of bank default

- Principal and interest paid and guaranteed by originator, not based on underlying asset performance

- Not true securitizations (no bankruptcy-remote structure; investors have recourse against originator)

-

-

Mortgage Pass-Through Securities:

-

Structure: True off-balance sheet securitizations where investors receive cash flows based entirely on pool performance less servicer fees

- Most are agency MBSs with implicit or explicit government guarantees

- Default risk minimal; primary risk is prepayment from refinancing after interest rate declines or home sales

-

Topic 1. Types of Structured Products

-

Collateralized Mortgage Obligations (CMOs):

- Structure: MBSs that tranche cash flows into different securities based on predetermined conditions, creating varied maturities and payment structures

- Waterfall/Sequential Pay Structure: Tranche 1 receives all principal and its interest portion until paid off; remaining tranches receive interest only until Tranche 1 retires, then principal flows sequentially to subsequent tranches

- Tranche 1 has lower prepayment risk than pass-throughs

-

Structured Credit Products:

-

Credit Risk Tranching: Pool backed by risky debt with tranches having different credit risk levels

- Junior (equity) tranches bear first losses from defaults

- Senior tranches have highest credit ratings and lowest write-down probability

- Losses cascade from junior to senior tranches sequentially

-

Topic 1. Types of Structured Products

-

Asset Backed Securities (ABSs):

- General Definition: Most general class where cash-flow generating assets are pooled and tranched; MBS is a special case of ABS

- Varieties: CBOs (collateralized bond obligations), CDOs (collateralized debt obligations), CLOs (collateralized loan obligations), CMOs, and complex structures like CDO-squared (CDO of CDOs)

- Key Variations:

- Collateral types: Loans, bonds, credit card receivables, auto loans, non-debt cash-flow instruments (e.g., toll collections)

- Tranche structure: Size and number specific to each transaction

- Management approach: Passive pools (assets pay down naturally) vs. actively managed pools (managers selectively add/remove assets to enhance performance)

- Revolving pools: Loan proceeds reinvested in new assets during revolving period; after period ends, balances fix and spend down (e.g., credit card balances)

Topic 2. Capital Structure in Securitization

- Capital Structure Hierarchy: Priority is assigned to tranches with senior tranches at the top receiving highest priority for principal and interest payments and lowest coupons due to perceived safety

- Equity Tranche:

- Lowest priority slice with first-loss absorption up to prespecified level

- No fixed coupon; receives residual cash flows after other claims satisfied

- Variable returns; typically smallest part of capital structure

- Mezzanine Tranche (Junior Tranche):

- Positioned between senior and equity tranches

- Absorbs losses only after equity tranche completely written down

- Attaches to equity from above and detaches from senior from below

- Offers relatively high coupon (fixed) or high spread (floating)

- Purposefully kept thin to maintain securitization viability

- Credit Enhancement Types: Risk protection mechanisms can be internal or external, with protection to some tranches shifting risk to other parts of capital structure

- External Credit Enhancement: Credit protection through insurance or wraps purchased from third parties, typically monoline insurers

Topic 2. Capital Structure in Securitization

- Internal Credit Enhancement - Overcollateralization:

- Hard credit enhancement available at pool origination

- Pool offers claims for less than collateral amount

- Example: 101 mortgages in collateral pool backing bonds totaling only 100 mortgages face value

- Internal Credit Enhancement - Excess Spread:

- Soft credit enhancement (zero at origination)

- Difference between cash flows collected and payments to bondholders

- Example: 8% weighted average collateral (net of fees) minus 7% weighted average payments = 1% residual

- Accumulates in separate trust account, invested and available for future shortfalls

Practice Questions: Q1

Q1. How many of the following statements concerning the capital structure in a securitization are most likely correct?

I. The mezzanine tranche is typically the smallest tranche size.

II. The mezzanine and equity tranches typically offer fixed coupons.

III. The senior tranche typically receives the lowest coupon.

A. No statements are correct.

B. One statement is correct.

C. Two statements are correct.

D. Three statements are correct.

Practice Questions: Q1 Answer

Explanation: B is correct.

Senior tranches are perceived to be the safest, so they receive the lowest coupon. The equity tranche receives residual cash flows and no explicit coupon. Although the mezzanine tranche is often thin, the equity tranche is typically the thinnest slice.

Topic 3. Waterfall Structure

- Basic Structure: Outlines rules governing collateral cash flow distribution to different tranches; senior and junior bonds receive promised coupons conditional on sufficient cash inflows from underlying loans, with residual cash flow called excess spread

- Overcollateralization Triggers: Determine how excess spread is divided between equity investors and accumulating trust; underlying cash flows are typically largest in early periods, allowing trust to build reserves against future shortfalls

- Complexity Factors:

- Structures may include a dozen or more tranches with different coupons, maturities, and overcollateralization triggers

- Loan defaults complicate the waterfall; actual default incidence affects tranche values relative to assumptions

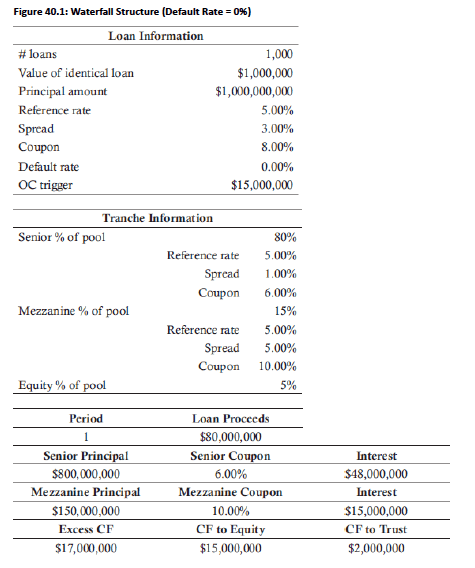

- Example Structure (1,000 loans × $1M each):

- Loan rate: Market reference rate + 300 bps (floating, annual reset)

- Senior tranche: 80% ($800M), spread = 1%, coupon = market rate + 1%

- Junior tranche: 15% ($150M), spread = 5%, coupon = market rate + 5%

- Equity tranche: 5% ($50M)

- Overcollateralization trigger: Equity capped at $15M maximum

Topic 3. Waterfall Structure

- 0% Default Rate Scenario (Fig 40.1):

- Total cash inflows: $1B × 8% = $80M (assuming 5% market reference rate)

- Senior coupon payment: $800M × 6% = $48M

- Junior coupon payment: $150M × 10% = $15M

- Residual: $80M - $63M = $17M

- Overcollateralization test: Equity receives maximum $15M, excess $2M flows to trust account

Topic 3. Waterfall Structure

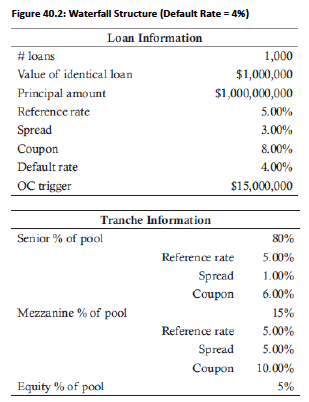

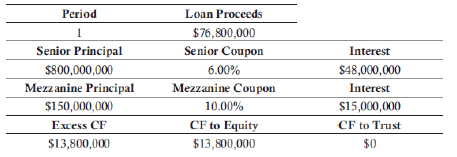

- 4% Default Rate Scenario (Fig 40.2):

- Total cash inflows: $1B × 8% × (1 - 0.04) = $76.8M

- Senior and junior bondholders paid in full ($48M + $15M = $63M)

- Equity tranche receives: $76.8M - $63M = $13.8M (below $15M maximum)

- No diversion to trust account as overcollateralization trigger not reached

Practice Questions: Q2

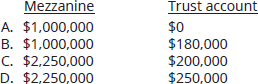

Q2. Assume there are 100 identical loans with a principal balance of $500,000 each. Based on a credit analysis, a 300 basis point spread is applied to the borrowers. The market reference rate is currently 4% and the coupon rate will reset annually. The senior, junior, and equity tranches are 75%, 20%, and 5% of the pool, respectively. The spreads on the senior and mezzanine tranches are 2% and 6%.

Excess cash flow is diverted above $1,000,000. Assume the default rate is 2%. What are the cash flows to the mezzanine and excess trust account in the first period?

Practice Questions: Q2 Answer

Explanation: A is correct.

The interest rate on the loans = 4% (market reference rate) + 3% (spread) = 7%. Therefore, the total collateral cash flows in the first period = 100 × $500,000 × 7% × (1 − 0.02) = $3,430,000. The senior tranche receives $50million × 0.75 × (4% + 2%) = $2,250,000. Similarly, the mezzanine tranche receives $50million × 0.20 × (4% + 6%) = $1,000,000. Next, the residual cash flows are calculated: $3,430,000 − $2,250,000 − $1,000,000 = $180,000. Since $180,000 < $1,000,000, all cash flows are claimed by the equity investors and there is no diversion to the trust account.

Module 2. Securitization

Topic 1. Securitization Participants

Topic 2. Three-Tiered Securitization Structure

Topic 1. Securitization Participants

- Originator/Sponsor: Funds the original loan; may be a bank, mortgage lender, or other financial intermediary; termed "sponsor" if supplying most of the collateral for the issue

- Underwriter: Structures the issue by engineering tranche sizes, coupons, and triggers; warehouses collateral and bears risks that the issue will not be marketed or that collateral value will decline; sells bonds to investors

- Credit Rating Agencies (CRAs): Provide credit ratings essential for investors to assess issue riskiness

- Influence tranche sizes by selecting attachment points and may require enhancements

- Face conflict of interest between profit generation and allocating larger portions to lower-interest senior notes

- Investors can mitigate concerns through independent analysis or purchasing insurance/wraps

- Servicer: Collects and distributes collateral cash flows and associated fees

- Provides liquidity for late payments and resolves defaults

- Faces conflict of interest in foreclosures (incentive to delay foreclosure to increase fees vs. investors' need for quick resolution)

- Manager (for actively managed pools):

- Has incentive to minimize effort in monitoring collateral credit quality

- Structure: Originator/manager bears first loss in capital structure to align incentives

- Custodians and Trustees: Play administrative role by verifying documents, disbursing funds, and transferring funds between accounts

Practice Questions: Q1

Q1. Which of the following participants in the securitization process is least likely to face a conflict of interest?

A. Credit rating agency and servicer.

B. Servicer and underwriter.

C. Custodian and trustee.

D. Trustee and manager.

Practice Questions: Q1 Answer

Explanation: C is correct.

The custodian and trustee play the least important roles in the securitization process. The servicer, originator, underwriter, credit rating agency, and manager all face conflicts of interest to varying degrees.

Topic 2. Three-Tiered Securitization Structure

-

Cash Flows in a three-tiered securitization (senior,mezzanine, and equity):

- Inflows from the collateral (Prior to Maturity): Interest on collateral (LtL_t Lt) plus recovery from defaulted assets (RtR_t Rt); collateral pool has NN N identical loans with coupons = market reference rate + spread

- Terminal Cash Flows: Last interest payment plus principal and recovery of defaulted assets; recovered funds from defaults earn interest at rate rr r over remaining pool life

- Outflows to the investors: Coupon payments to senior and mezzanine noteholders (denoted BB B, assumed constant); equity holder cash flows depend on inflows - funds diverted to excess spread account

-

Overcollateralization (OC) Determination Process: Let denotes the amount diverted to the spread trust in year t, with maximum allowable diversion K.

- Step 1 - Interest Sufficiency: If Lt−B≥0L_t - B ≥ 0 Lt−B≥0 (interest covers current-period coupons):

- If Lt−B≥KL_t - B ≥ K Lt−B≥K: Divert KK K to trust, flow Lt−B−KL_t - B - K Lt−B−K to equity holders (OCt=KOC_t = K OCt=K)

- If Lt−B<KL_t - B < K Lt−B<K: Divert Lt−BL_t - B Lt−B to trust, nothing flows to equity holders (OCt=Lt−BOC_t = L_t - B OCt=Lt−B)

- Step 2 - Interest Shortfall: If Lt−B<0L_t - B < 0 Lt−B<0 (interest insufficient to cover current-period coupons):

- All LtL_t Lt flows to bondholders with shortfall = B−LtB - L_t B−Lt

- Check if accumulated trust funds cover shortfall; if yes, bondholders paid in full; if no, bondholders suffer write-down

- Step 1 - Interest Sufficiency: If Lt−B≥0L_t - B ≥ 0 Lt−B≥0 (interest covers current-period coupons):

Topic 2. Three-Tiered Securitization Structure

-

Default and Recovery Calculations: Assume 40% recovery rate.

-

Recovery Amount:

-

where number of defaults in period t

-

-

Total Trust Deposit:

-

Accumulated Trust Account Balance:

-

-

-

-

Shortfall Coverage Test:

-

-

- If true: Trust makes bondholders whole

- If false: Fund reduced to 0, bondholders receive trust account balance

-

-

- Amount diverted to the Overcollateralization Account:

-

-

- Upper condition: Inflows to trust account

- Lower condition: Outflows from trust account

-

Topic 2. Three-Tiered Securitization Structure

-

Equity Cash Flows:

-

Terminal Year Examination: Surviving loans return principal, no OC diversion (structure ends), no need to test OC triggers since there is no diversion to the trust

-

- Terminal Cash Flow Components:

-

Loan Interest:

-

-

-

-

Principal Redemption:

-

-

-

-

Final Recovery:

-

-

-

Residual Trust:

-

-

-

-

-

Waterfall Distribution of Terminal Cash Flows:

- Senior Tranche Priority: Sum of terminal cash flows is first compared to the amount due to senior tranche; if sufficient, senior tranche is paid off and remainder flows down the capital structure

- Junior Tranche Payment: If remainder after senior tranche payment is large enough to cover junior tranche obligations, junior tranche is paid and residual flows to equity holders

- Insufficient Funds Scenario: If remainder cannot meet junior tranche claims, junior bondholders receive only the available excess and equity holders receive nothing

Topic 2. Three-Tiered Securitization Structure

-

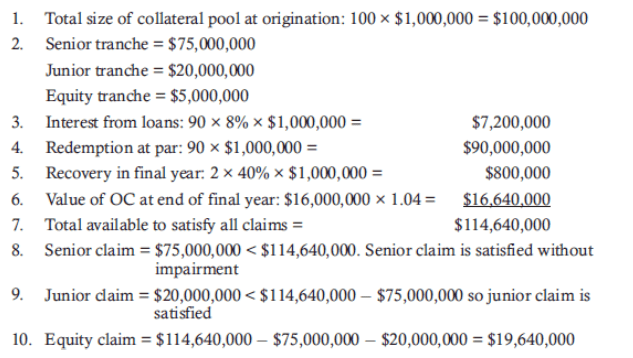

Example 1: Determine the terminal cash flows to senior, junior, and equity tranches given the following information. The original loan pool included 100 loans with $1 million par value and a fixed coupon of 8%. The number of surviving loans is 90. The par for the senior and junior tranches is 75% and 20%, respectively. The equity investors contributed the remaining 5%. There were two defaults with recovery rate of 40% recovered at the end of the period. The value of the trust account at the beginning of the period is $16million earning 4% per annum.

Topic 2. Three-Tiered Securitization Structure

-

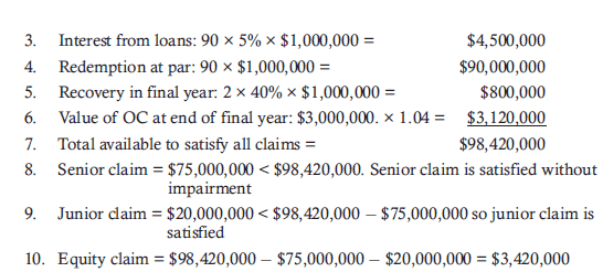

Example 2: Now, continue with the same example, but change the interest rate to 5% and the beginning OC value to $3million. The first two steps will be the same as before.

Topic 2. Three-Tiered Securitization Structure

-

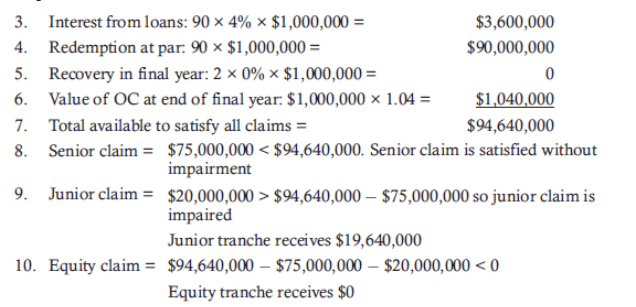

Example 3: Finally, continue with the same example, but change the interest rate to 4% and the beginning OC value to $1million. Assume a recovery rate of zero. Again, the first two steps are the same as before.

Topic 2. Three-Tiered Securitization Structure

Module 3. Simulation, PD and Default Correlation; Default Sensitivities; and Structured Products

Topic 1. Credit Losses Simulation Approach

Topic 2. Impact of PD and Default Correlation

Topic 3. Measuring Default Sensitivities

Topic 4. Risks for Structured Products

Topic 5. Implied Correlation

Topic 6. Structured Products Motivations

Topic 1. Credit Losses Simulation Approach

- Key Simplifying Assumptions in Basic Analysis: Constant default rates year-over-year, identical default probabilities across loans, and ignored loan correlations; simulation is required to incorporate these realistic factors into the analysis

- Step 1: Estimate the Parameters

- Estimate default intensity using market spread data to infer hazard rates across various maturities

- Estimate pairwise correlations (challenging due to lack of usable market data); copula correlation theoretically useful but lacks empirical precision in practice

- Perform sensitivity analysis for various default and correlation pairs

- Step 2: Generate Default Time Simulations: Identify if and when each security defaults; simulation provides timing information for each hypothetical outcome

- Step 3: Compute Portfolio Credit Losses

- Use simulation output to determine frequency and timing of credit losses

- Align credit losses to assess impact on capital structure losses

- Identify credit VaR for each tranche using the tail of the distribution

Topic 2. Impact of PD and Default Correlation

- Impact of Probability of Default (PD): For a given correlation level, increasing probability of default negatively affects cash flows and values across all tranches

- Key Insight: Correlation is generally a more important risk factor than default probability, which may not be entirely intuitive.

- Correlation Effects by Tranche Type:

-

Low Correlation Scenario: When correlation approaches zero, loan defaults are independent; in large portfolios, defaults cluster near mathematical expectation (analogous to coin flips: 1,000 flips yield ~500 heads, rarely <400 or >600), making senior tranches unlikely to be impaired

- Senior Tranche: Increasing correlation reduces tranche value as losses become more clustered and extreme, with the impact becoming stronger at higher default probabilities.

- Equity Tranche: Higher correlation increases value by raising the chances of very low or no defaults, while low correlation leads to more predictable losses and write-downs.

- Mezzanine Tranche: Correlation has a mixed impact - at low default rates it increases losses (reducing value), while at high default rates it reduces expected losses, leading to higher value.

-

Topic 2. Impact of PD and Default Correlation

- Convexity Characteristics:

- Equity Tranches: Exhibit positive convexity; as defaults increase from low levels, values decrease rapidly then moderately (thin tranche structure causes disproportionate initial price impact)

- Senior Tranches: Exhibit negative convexity; as defaults increase, bond price declines accelerate

- Mezzanine Tranches: Mixed convexity profile- negative at low default rates, positive at high default rates

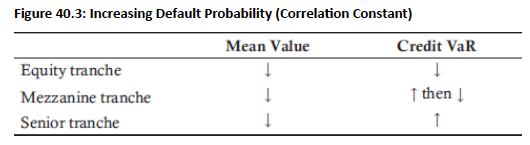

- Credit VaR Analysis: Default Probability Impact (Fig 40.3):

- Equity tranches: Increasing default probability generally decreases VaR (less return variation)

- Senior tranches: Increasing default probability increases VaR (more return variation)

- Mezzanine tranches: Mixed effect—VaR increases at low correlation levels (like senior), decreases at high correlation levels (like equity)

Topic 2. Impact of PD and Default Correlation

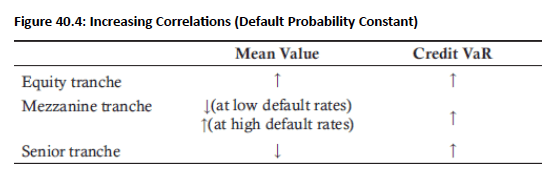

- Rising Correlation Impact (Fig 40.4):

- Senior Tranches: VaR increases with correlation as clustered defaults make subordination more likely to be breached, though the incremental rise at very high correlations (e.g., 0.6 vs 0.9) is limited. At low correlation and even high default rates, senior tranches remain well protected due to subordination (e.g., 10%), but at higher correlations (≥0.6), VaR becomes relatively insensitive to PD.

- Equity Tranches: Returns improve as the probability of low-default scenarios increases, which is more likely at higher correlations compared to low correlation environments where defaults are more certain. However, as correlation approaches one, equity tranche VaR rises steadily, reflecting higher expected returns alongside greater risk and variability.

- Mezzanine Tranches: At low default rates and low correlations, mezzanine tranches behave similarly to senior tranches with relatively low VaR. However, as PD and/or correlations increase, their risk profile shifts and begins to resemble that of equity tranches, showing significantly higher sensitivity to losses.

Practice Questions: Q1

Q1. Which of the following statements about portfolio losses and default correlation are most likely correct?

I. Increasing default correlation decreases senior tranche values but increases equity tranche values.

II. At high default rates, increasing default correlation decreases mezzanine bond prices.

A. I only.

B. II only.

C. Both I and II.

D. Neither I nor II.

Practice Questions: Q1 Answer

Explanation: A is correct.

Statement I is true. Increasing default correlation increases the likelihood of more extreme portfolio returns (very high or very low number of defaults). The increased likelihood of high defaults negatively impacts the senior tranche. On the other hand, the increased likelihood of few defaults benefits the equity tranche as it bears first loss.

Statement II is false. At high default rates, increasing the correlation increases the likelihood of more extreme portfolio returns which benefits equity investors and mezzanine investors.

Topic 3. Measuring Default Sensitivities

- Default '01 Definition: Extension of DV01 concept to default probabilities; measures tranche sensitivity by shocking default probability up and down by 10 basis points (0.001) and revaluing through VaR simulations

- Default '01 Formula:

- Non-Linear Relationship: The effect of increasing default probability on tranche values is not necessarily linear and depends on interaction with default correlation

- Qualitative Impacts:

- Always positive for any default probability-correlation combination (all tranches negatively affected by increasing default probabilities)

- Approaches zero as default rates become sufficiently high (marginal impact diminishes)

- Maximum variation occurs when default rate generates losses close to tranche's attachment point (similar to high gamma for at-the-money options)

Topic 4. Risks for Structured Products

- Systematic Risk: Similar to equity portfolios, credit portfolios cannot eliminate systematic risk even with well-diversified collateral pools across lenders, terms, and geography

- High systematic risk (expressed through high correlations) can severely damage portfolios

- Increased pairwise correlations raise the likelihood of senior tranche write-downs

- Tranche Thinness: Equity and mezzanine tranches are relatively thin, resulting in narrow gaps between credit VaR levels (e.g., 95% and 99% VaR are closely positioned)

- Implication: Once a tranche is breached, the resulting loss is likely to be very large

- Loan Granularity: Refers to loan-level diversification within the portfolio

- Example: MBS pools with few large loans versus many smaller loans

- Reduced sample size (fewer, larger loans) increases the probability of tail events compared to equal-sized portfolios with more loans of smaller amounts

Topic 5. Implied Correlation

- Concept Similarity to Implied Volatility: Implied correlation parallels implied volatility in equity options; both use observable market prices and accepted valuation models to back out unique unobserved parameters (volatility for options, correlation for tranches)

- Calculation Process: Observable market prices combined with tranche pricing functions allow extraction of unique implied correlation to calibrate model prices with market prices

- Mechanical Steps:

- Extract risk-neutral default probabilities and recovery rates from observable CDS term structure

- Input default estimates and correlation estimates into a copula assuming constant pairwise correlation and market prices

- Output risk-neutral implied correlation (base correlation) per tranche

- Correlation Skew: Correlation estimates vary between tranches and are not constant, creating correlation skew across the capital structure

- Example Application: If equity tranche market price increases from $3 million to $3.2 million while risk-neutral default probabilities remain constant, the market's implied correlation estimate must have increased (higher correlations benefit equity holders)

Practice Questions: Q2

Q2. Which of the following statements best describes the calculation of implied correlation?

A. The implied correlation for the mezzanine tranche assumes non-constant pairwise correlation.

B. Observable market prices of credit default swaps are used to infer the tranche values.

C. The tranche pricing function is calibrated to match the model price with the market price.

D. The risk-adjusted default probabilities are used in model calibration.

Practice Questions: Q2 Answer

Explanation: C is correct.

Starting with observed market prices and a pricing function for the tranches, it is possible to back out the implied correlation to calibrate the model price with the market price. The computation of implied correlation assumes constant pairwise correlation. Both credit default swap and tranche values are observed. Observed tranche values are used in conjunction with risk-neutral default probabilities to compute implied correlation.

Topic 6. Structured Products Motivations

-

Loan Originator Motivations:

-

Lower Cost of Funding: Securitization provides cheaper financing than retaining loans or selling in secondary markets due to diversification of loan pools and originator's reputation for high-quality underwriting

- Diversification Challenges: Some loan pools (e.g., commercial mortgages) are difficult to diversify, leaving systematic risk that may lead to underestimation of overall risk

- Servicing Fee Income: Originators collect ongoing servicing fees as an additional benefit beyond the funding cost advantage

-

-

Investor Motivations

-

Access to Diversified Loan Pools: Investors gain exposure to diversified loan portfolios (e.g., mortgages, auto loans) not otherwise accessible without securitization

- Customizable Risk-Return Profiles: Tranching structure allows investors to select desired risk-return levels:

- Equity tranches: Higher risk-return

- Senior tranches: Lower risk-return

- Due Diligence Requirement: Investors must conduct proper analysis of potential tranche investments to understand actual risk levels and avoid mispricing

-