Book 5. Risk and Investment Management

FRM Part 2

IM 13. Private Capital Investing: Distress Symptoms and Remedies

Presented by: Sudhanshu

Module 1. Understanding Financial Distress

Module 2. Remedies and Legal Challenges in Financial Distress

Module 1. Understanding Financial Distress

Topic 1. Early Warning Signals of Financial Distress

Topic 2. Indicators of Financial Distress

Topic 3. Causes of Financial Distress

Topic 1. Early Warning Signals of Financial Distress

-

Early detection is critical but often difficult because it can be hard to distinguish between symptoms of distress and underlying problems, or to tell if changes are temporary fluctuations or permanent issues.

-

Key Accounting Assessment Questions: To identify distress early, analysts should evaluate the following core accounting questions:

-

Core Operations: Are earnings being generated from core operations?

-

Accounting Policies: Do current policies artificially increase profitability?

-

Reserves: Have there been any changes in reserve accounting policies?

-

Adjustments: Are there any restructuring or reorganization adjustments?

-

Creditor Behavior: Are creditors showing signs of concern?

-

Bad Debts: Are bad debts being written off?

-

Taxation: Does the tax charge appear low relative to reported earnings?

-

Topic 2. Indicators of Financial Distress

-

Classification of Distress Indicators: The symptoms of credit deterioration are primarily categorized into financial and nonfinancial indicators.

-

Financial Indicators: These involve quantitative breaches or accounting maneuvers used to mask performance:

-

Covenant Breaches

-

Late submission of financial statements.

-

Use of Creative Accounting (e.g., off-balance-sheet financing or contingent liabilities).

-

Earnings Enhancements (e.g., sale-leaseback arrangements, asset write-downs followed by gains on sale, accelerated revenue recognition, or deferral of costs)

-

-

Nonfinancial Indicators: These involve qualitative changes in corporate behavior or structure:

-

Unnecessarily complex corporate structure

-

Resignations of board members or senior management

-

Change in the firm’s fiscal year-end date

-

Change in auditors

-

Failure to meet commitments in a timely manner

-

Material changes in risk tolerance

-

Practice Questions: Q1

Q1. Which of the following is a clear financial indicator of credit deterioration?

A. Change in auditors.

B. Material changes in risk tolerance.

C. Use of a sale-leaseback arrangement.

D. Board or senior management resignations.

Practice Questions: Q1 Answer

Explanation: C is correct.

Financial indicators include covenant breaches, late submission of financial statements, creative accounting practices, and earnings enhancements such as sale-leaseback arrangements. Nonfinancial indicators include unnecessarily complex corporate structures, management resignations, changes in fiscal year-end date or auditors, failure to meet commitments, and material changes in risk tolerance.

-

Financial defaults and distress can stem from various sources, including unsuitable business models, excessive leverage, overly complex organizational structures, or internal/external shocks. These causes are generally categorized into the following five areas.

-

Leverage and Business Performance

- Excessive Leverage + Solid Business: Debt fully drawn; triggered by cyclical downturn; cash flows stabilize ~10% below default point; revenue recovery within 3 years

- Average Leverage + Weak Operations: Significant revenue and margin declines; default during or independent of downturn; cash flows fall >50% below default point; recovery takes 5-10 years

- Excessive Leverage + Weak Operations: Debt fully drawn with substantial revenue/margin drops; cyclical trigger likely; cash flows decline ≥70% below default; extended recovery period

-

Unexpected Liabilities

-

Tort Liabilities: Legal claims from harm to individuals/property, often through class action lawsuits; typically underestimated by management; awards frequently exceed expectations; insurance coverage uncertain; markets discount prices accordingly

- Contract Liabilities: Contractual arrangements become unfavorable due to changed circumstances; risks often inherited through acquisitions; problematic terms unknown in advance make protection difficult

-

Topic 2. Causes of Financial Distress

-

Performing Below Expectations

- Economic Downturns: Unavoidable business cycle recessions; key challenge is distinguishing cyclical effects from poor management decisions and strategies

- Uncompetitive Products/Services: Evolving demand and shifting customer preferences render existing offerings obsolete

-

Crisis of Confidence

-

Reliability of Historical Information: Financial fraud makes all previously reported data suspect; must assess informational contagion potential and determine practical data reliability cutoff point

- Liquidity and Bankruptcy Risk: Evaluate whether fraud triggers liquidity problems or bankruptcy risk; key factors include cash balances, credit line availability, and loan acceleration risk

-

- Unrealistic Business Plans

- Leveraged Buyouts: Assumes sufficient cash generation through asset sales or operations to reduce leverage; distress occurs when expectations unmet

- Roll-ups: Consolidation strategy relies on anticipated economies of scale; expected cost savings often fail to materialize

- Excessive New Entrants: High margins attract multiple firms to new industry; oversupply when entrants exceed underlying demand creates problems for all competitors

Topic 2. Causes of Financial Distress

Practice Questions: Q2

Q2. Which of the following scenarios is most likely to result in a rapid, deep cash flow decline and a prolonged period before revenue recovery?

A. Average leverage with weak business operations.

B. Minimal leverage and strong business performance.

C. Excessive leverage combined with a solid business model.

D. Excessive leverage combined with weak business operations.

Practice Questions: Q2 Answer

Explanation: D is correct.

When excessive leverage is combined with weak business operations, cash flows can fall 70% or more below the point of default, and revenue recovery can take an extended period—often beyond 10 years.

Module 2. Remedies and Legal Challenges in Financial Distress

Topic 1. Restructuring

Topic 2. Raising Additional Capital

Topic 3. Reducing Leverage

Topic 4. Practical Limitations

Topic 5. Legal Challenges During Financial Distress

Topic 6. Out-of-Court Restructurings (OCRs)

Topic 7. In-Court Restructurings (ICRs)

Topic 8. Key Legal Risks

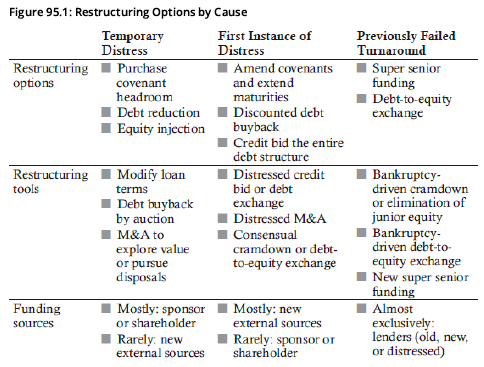

Topic 1. Restructuring

-

Restructuring is one of three primary solutions to financial distress, alongside raising additional capital and reducing leverage.

-

The appropriate restructuring approach depends on:

-

Temporary Distress: Whether the performance deterioration is temporary,

-

First Instance of Distress: Whether the firm is experiencing distress for the first time,

-

Previously Failed Turnaround: Whether a previous turnaround effort has already failed.

-

Topic 1. Restructuring

-

Debt Trading Level as Distress Indicators

- Market Insight: When a firm's debt is actively traded, the trading level provides valuable insight into underlying financial issues and the range of potential restructuring solutions

- Trading Level Definition: Debt trading level reflects the current market price of the firm's debt relative to its full repayment value (par value)

- Distress Signal: The trading level serves as a market-based indicator of distress severity and expectations about potential restructuring options.

Topic 2. Raising Additional Capital

- Purpose and Risk: Raising capital may not resolve underlying problems but buys time for the business to work through difficulties or for conditions to improve; however, it may also allow ineffective management to further erode value

- Common Ways to raise extra cash:

- Asset Sales: Timing is critical as firms can typically secure prices above fair market value more easily before bankruptcy filing; price considerations are essential for distressed investors evaluating this option

- Secured Financing: Firms may borrow against unencumbered assets (not already pledged as collateral); however, this option is often limited as the most valuable assets have usually been pledged during earlier restructuring efforts

- Sale-Leaseback: Firm sells an asset to investors and immediately leases it back, providing capital infusion while preserving operational access; leases may be structured off-balance sheet to make leverage appear lower

- Equity Sponsor: Private owners with majority stake (>50%) are generally positive for distressed investors as they only realize value after debt claims are satisfied, aligning incentives; this dynamic is difficult to achieve in public firms with dispersed ownership

Practice Questions: Q1

Q1. Which of the following methods most effectively provides cash to a distressed firm while allowing it to continue using a key operational asset?

A. Asset sale.

B. Equity sponsor.

C. Sale-leaseback.

D. Secured financing.

Practice Questions: Q1 Answer

Explanation: C is correct.

A sale-leaseback allows the firm to sell an asset for immediate cash and then lease it back, preserving operational use while improving liquidity. Asset sales remove access to the asset entirely. Secured financing is often not feasible because distressed firms typically have few unencumbered assets available for collateral. Equity sponsorship can provide cash, but it does not directly preserve the use of a specific asset and can be difficult to secure.

Topic 3. Reducing Leverage

-

Solution to Financial Distress: Reducing leverage is a primary solution for addressing financial distress. This is achieved by either increasing equity or decreasing debt.

-

Increasing Equity: Can be arranged quickly from incumbent investors, while new investors require longer due diligence; often required by lenders as part of restructuring

-

Decreasing Debt:

-

Open Market Repurchases: Most effective for retiring less than 20% of outstanding bonds; simple, fast, low-cost, and discreet approach with bonds typically repurchased at a discount; lenders often require repaying bank debt before nonbank debt

- Direct Purchases from Bondholders: Firm negotiates individually with bondholders who seek higher prices than available in the open market

- Cash Tender Offer: Used for retiring large portions of outstanding debt; available to all bondholders with strict terms including acceptance deadline, purchase price, and maximum buyback amount

- Exchange Offer: For cash-constrained firms; offers new securities in exchange for existing distressed debt; can be coercive (warning nonparticipants of disadvantages) or noncoercive (highlighting opportunity attractiveness)

-

Practice Questions: Q2

Q2. Which of the following scenarios is the most effective situation for using open market repurchases to reduce a company’s debt?

A. The firm wants to offer alternative securities instead of cash.

B. The firm wants to repurchase only a small percentage of its outstanding bonds.

C. The firm needs to reduce a large proportion of its total debt under strict offer conditions.

D. Individual bondholders approach the firm directly, seeking smaller discounts than the market price.

Practice Questions: Q2 Answer

Explanation: B is correct.

Open market repurchases are most effective when the firm intends to repurchase a relatively small amount of debt, typically less than 20% of outstanding bonds. They are fast, low cost, and discreet. Larger reductions in debt are better handled through a cash tender offer, while direct purchases from bondholders and exchange offers apply in other situations.

Topic 4. Practical Limitations

-

The most common restructuring limitations include the following:

-

Liquidity: The easiest path to deleveraging, such as buying back debt at a discount, may not be feasible if the firm lacks sufficient excess cash.

-

Timing: It is important to consider the time until the next expected liquidity event. Some methods of raising cash are not viable if the firm needs liquidity quickly. For example, selling a business unit can take a significant amount of time.

-

Magnitude: The severity of the problem depends on both time and available resources. A short time horizon combined with limited liquidity can turn a small issue into a major one.Complexity.

-

Complexity: Restructuring becomes more difficult as the capital structure becomes more layered. A large amount of secured bank debt can limit options because of restrictive covenants. All key provisions and covenants must be understood when evaluating a distressed firm’s options.

-

Severability: Some firms have both core and noncore business units. Noncore units may be sold to reduce leverage without harming the core business. Firms with only core operations often lack this flexibility.

-

Practice Questions: Q3

Q3. Which of the following statements best describes a key limitation that can prevent a distressed firm from executing a theoretical restructuring strategy?

A. A firm can always sell any business unit immediately to raise cash.

B. A firm with limited cash reserves may be unable to repurchase debt.

C. The presence of noncore business units always reduces restructuring risk.

D. Firms with simple capital structures typically face significant restructuring challenges.

Practice Questions: Q3 Answer

Explanation: B is correct.

Limited liquidity often prevents a distressed firm from pursuing an otherwise viable restructuring strategy, such as repurchasing debt at a discount. Other limitations include the time required to sell business units, the magnitude of the liquidity shortfall, the complexity of multilayered capital structures, and the inability to divest core operations.

Topic 5. Legal Challenges During Financial Distress

- Restructuring Complexity: Companies undergoing restructuring face complex legal, tax, and accounting issues that require careful navigation and specialized expertise

- Court vs. Non-Court Options: Debt can be restructured either with or without court supervision; court-supervised processes tend to be time-consuming, costly, and potentially damaging to the firm's reputation

- Two Primary Approaches: Out-of-court restructurings (negotiated directly with creditors) and in-court restructurings (formal bankruptcy or insolvency proceedings under judicial oversight)

Topic 6. Out-of-Court Restructurings (OCRs)

-

In an Out-of-Court Restructuring (OCR), a distressed company and its creditors bypass formal court supervision to negotiate directly and modify the terms of existing financial obligations. This process is characterized by voluntary exchanges of financial interests and is generally faster and less costly than in-court alternatives.

-

Key Elements and Parties Involved

The success of an OCR depends on identifying and negotiating with the correct representatives for different types of debt:

-

Bank Debt: If held by a single lender or a small group, the process is straightforward. For syndicated loans, a designated agent typically leads the negotiations.

-

Bondholders: Because bond ownership can be widely dispersed, key investors usually form a bondholder committee to negotiate.

-

Indenture Trustees: While they are the formal representatives of the bonds, they typically seek broad consensus among holders to minimize legal risk.

-

- Implementation of Changes

The ease of implementing agreed-upon terms varies by the type of instrument being restructured:

Topic 6. Out-of-Court Restructurings (OCRs)

-

Voluntary Negotiation: Company and creditors negotiate directly to modify existing obligations through voluntary exchange of financial interests, without court involvement

-

Parties Involved

-

Bank Debt: Single lenders or small groups negotiate directly; syndicated loans are led by a designated agent

- Bondholder Representation: Key investors form a bondholder committee to negotiate; indenture trustee serves as formal representative but typically seeks broad consensus before acting to minimize legal risk

-

-

Implementation of Changes

-

Bank Loans: Relatively straightforward; holders of majority bank debt can approve most amendments binding all lenders, though unanimous consent required for material changes (maturity dates, interest rates, collateral)

- Bonds: Quick execution if bondholder committee agrees; broader participation may require formal exchange or tender offer, demanding significant time and effort

-

-

Feasibility and Holdout Problem

-

Voluntary Participation Risk: OCR can fail if creditors hold out believing they may receive better terms than cooperating creditors; excessive holdouts can trigger costly bankruptcy leaving all parties worse off

- Holdout Mitigation: Implied threat of future economic leverage in repeat dealings can discourage obstructionist behavior, as creditors blocking one transaction may face unfavorable treatment in future negotiations

-

Topic 6. Out-of-Court Restructurings (OCRs)

-

Coercive Mechanisms in Debt Restructuring

-

Covenant Stripping: Tender offers may include clauses that remove protective covenants from bonds held by nonparticipating creditors once the majority accepts the offer, pressuring holdouts to participate

- Prepackaged Bankruptcy Threat: Combining an exchange offer with a request to support prepackaged bankruptcy makes the bankruptcy threat credible and streamlines the process if restructuring fails

- Expedited Process: Prepackaged bankruptcies can sometimes be completed in less than six weeks, providing a faster resolution than traditional bankruptcy proceedings

-

Topic 7. In-Court Restructurings (ICRs)

-

Court-Managed Bankruptcy

- Market Signaling: Companies typically signal imminent bankruptcy filing to financial markets, allowing investors to prepare for potential losses; experienced distressed debt investors form views on whether firms will pursue out-of-court restructuring (OCR) or in-court restructuring (ICR)

- Filing Considerations: Bankruptcy officially begins when a petition is filed with the bankruptcy court; strategic decisions involve both timing of filing and choice of jurisdiction

-

Four Primary Chapter 11 Objectives

- Operational Stabilization: Secure liquidity needed to continue functioning after the petition is filed and stabilize day-to-day operations

- Business Plan Development: Create a forward-looking plan designed to maximize firm value and/or asset value

- Liability Identification: Identify all liabilities and determine their legal priority in the capital structure

- Capital Structure Reorganization: Establish a new capital structure for the reorganized firm

Topic 7. In-Court Restructurings (ICRs)

-

Reorganization Plan and Claim Classes: Chapter 11 requires a reorganization plan (legal document) outlining treatment of all stakeholders and liabilities; claimants are grouped into classes based on similar characteristics, with all class members receiving equal treatment

- Class 1 - Administrative Claims: Post-petition fees and costs of lawyers, accountants, and other professional advisors

- Class 2 - Super Secured Claims (DIP Financing): Debtor-in-possession financing amounts; receives priority over all other claims

- Class 3 - Priority Claims: Allowed amounts payable to employees for pre-petition obligations

- Class 4 - Super Secured Claims (Pre-Petition Secured Lenders): Pre-petition claims of senior secured lenders and secured noteholders

- Class 5 - Senior Unsecured Claims: Pre-petition claims of trade creditors, senior unsecured lenders, and unsecured noteholders

- Class 6 - Equity: Equity interests of pre-petition shareholders (typically last in priority)

Practice Questions: Q4

Q4. Which of the following statements best captures a key difference between out-of-court restructurings (OCRs) and in-court restructurings (ICRs)?

A. OCRs are typically faster, while ICRs can be slower.

B. OCRs eliminate the risk of holdouts among creditors.

C. ICRs avoid reputational damage for the distressed firm.

D. ICRs are always preferred by creditors because they offer more flexibility.

Practice Questions: Q4 Answer

Explanation: A is correct.

OCRs rely on voluntary negotiation and are generally faster and less costly to execute, but they introduce the risk of creditor holdouts. ICRs involve formal court supervision, which can be slower, more expensive, and potentially damaging to the firm’s reputation.

Topic 8. Key Legal Risks

- Stakeholder Dynamics: Distressed investors must understand the roles and negotiation leverage of each party involved in the bankruptcy process, requiring strategic thinking and tactical maneuvering

- Creditor Risk Hierarchy: Unsecured creditors face the highest risk among debtholders due to lack of collateral protection

- Critical Risks: There are three critical risks which investors should understand:

-

Stay on claims: The bankruptcy court can temporarily prevent creditors from collecting on their claims or enforcing their collateral.

-

Preference (twilight) period: The court reviews transactions made shortly before the bankruptcy to ensure that no creditor class was improperly favored over others.

-

Upstream guarantees: These occur when a subsidiary guarantees the debt of its parent company. Some jurisdictions restrict the use of upstream guarantees, while others provide limited or unclear guidance.

-