Book 5. Risk and Investment Management

FRM Part 2

IM 8. Hedge Fund Investment Strategies

Presented by: Sudhanshu

Module 1. Equity-Based and Macro Strategies

Module 2. Arbitrage Strategies

Module 3. Event-Driven and Distressed Strategies

Module 1. Equity-Based and Macro Strategies

Topic 1. Equity Long/Short Strategy

Topic 2. Dedicated Short (Short-Biased) Strategy

Topic 3. Nonhedged Equity Strategy

Topic 4. Global Macro Strategy

Topic 5. Emerging Markets Strategy

Topic 1. Equity Long/Short Strategy

-

Overview: Equity long/short strategies rely heavily on deep fundamental research, evaluating company risks and opportunities across industry conditions, geographic exposure, and macroeconomic trends to identify mispriced securities.

-

Long and Short Positioning: The strategy involves taking long positions in undervalued stocks and short positions in overvalued ones, allowing managers to capture relative mispricing while reducing overall market exposure.

-

Alpha Generation Through Selection: Strong security selection is the primary driver of alpha, as managers aim to profit from valuation convergence rather than market movements.

-

Investment Horizon Planning: Managers define an investment horizon for each position, representing the expected time required for the market price to converge to their valuation estimate.

-

Event-Driven Opportunities: Funds may exploit corporate events such as mergers or takeovers, building long positions in firms that are likely acquisition targets to benefit from anticipated price revaluation.

-

Short Position Risk Management: Short positions carry unique risks such as margin calls and short squeezes, so managers carefully monitor holding periods and price movements to limit potential losses.

-

Diversification and Factor Control: To control risks, managers limit individual short exposures (typically 2–3% of fund capital) and use factor models to neutralize residual exposures beyond market beta.

Topic 1. Equity Long/Short Strategy

-

Financial Components: The performance of this strategy is determined by specific return sources and costs.

-

Sources of Return:

-

Alpha Returns: Profits generated from both the long and short positions.

-

Interest Rebate: Interest earned on the cash proceeds from short sales, net of fees paid to brokers and securities lenders.

-

Liquidity Buffer Interest: Interest earned on the cash posted at the start of the strategy to cover daily MTM adjustments.

-

-

Costs:

-

Financing and Fees: Charges on margin loans, fees for borrowing shares for short positions, and dividends that must be paid to the lender for borrowed shares.

-

Transaction Costs: Costs associated with executing trades.

-

Practice Questions: Q1

Q1. Which of the following hedge fund strategies is most likely to earn an interest rebate as a source of income?

A. Global macro.

B. Equity long/short.

C. Emerging markets.

D. Nonhedged equity.

Practice Questions: Q1 Answer

Explanation: B is correct.

Equity long/short strategies establish short positions, and the cash proceeds from these short sales can earn an interest rebate. The other strategies do not typically rely on short sale proceeds as a primary income source.

- Overview: Dedicated short strategies concentrate on identifying overpriced securities and selling them short to profit from price declines

- Inherent Risks: This approach carries significant risks including potential margin calls, short squeezes where rapid price increases force covering, and forced position closures driven by risk management constraints

- Market Opportunity - Limited Competition from Long-Only Managers in Mutual Funds:

- Mutual funds primarily focus on identifying positive-alpha stocks and typically do not take short positions

- Long-only managers may underweight negative-alpha stocks but provide limited attention to overvalued securities

- This creates opportunities for short specialists to exploit mispricings in overvalued names

- Short Seller Expertise: Dedicated short managers develop specialized skills in identifying signs of overvaluation such as aggressive accounting practices, potential legal issues, or management attempts to obscure negative information

- Structural Challenge: Market prices tend to rise over time, creating an inherent headwind and bias toward negative returns on short positions; without specialized expertise or insights, short sellers are likely to lose money while assuming significant risk

Topic 2. Dedicated Short (Short-Biased) Strategy

Practice Questions: Q2

Q2. Which of the following statements best describes the primary risk associated with a dedicated short strategy?

A. Lack of leverage prevents meaningful alpha generation.

B. Short sale proceeds generate insufficient interest rebates to offset costs.

C. Market prices tend to decline over long periods, limiting upside potential.

D. Rising share prices can trigger margin calls and forced covering of positions.

Practice Questions: Q2 Answer

Explanation: D is correct.

Dedicated short strategies face significant risk from rising share prices, which can lead to margin calls, short squeezes, and forced covering.

- Overview: Relies on fundamental analysis with a long-only focus on individual firms or industries, resembling traditional stock-picking approaches without hedging positions

- Mutual Fund Approach - Diversification Focus: Emphasizes expected returns and uses portfolio diversification for risk management; may skip detailed analysis of investments with minimal expected returns due to resource constraints

- Hedge Fund Approach - Concentrated Analysis: Can concentrate on individual stocks and evaluate both upside and downside potential; often bypasses investments too small for mutual fund analysis

- Leverage Amplification: Uses significant leverage to amplify returns from even small mispricings in securities

- Bull Call Spread Example: Manager buys a call option with lower strike price and sells a call with higher strike price; generates enhanced returns even with modest 10-15% stock price increases

Topic 3. Nonhedged Equity Strategy

- Overview: Makes large, leveraged bets on anticipated price movements across equity, fixed-income, interest rates, foreign exchange, and commodities markets.

- Derivative Positions: Takes derivative positions including options, swaps, and futures linked to a wide range of underlying asset classes and indices.

- Investment Flexibility: Unlike mutual funds with restricted mandates, global macro funds have broad discretion in selecting opportunities across global markets without sectoral or geographic constraints.

- Strategy Objective: Managers attempt to anticipate changes in international macroeconomic trends and take large positions to generate substantial profits through flexible capital allocation across sectors, regions, and asset classes.

- Analysis Framework: Considers a wide range of factors including:

- Economic forecasts and trends

- International capital flows

- Interest rate movements

- Political developments and government relationships

- Economic policies

- Other broad market-influencing forces

- Liquidity Preference: Tends to trade in more liquid instruments to enable rapid position adjustments and efficient execution of large-scale trades.

Topic 4. Global Macro Strategy

- Investment Focus: Strategy involves investing in securities of developing countries, encompassing both corporate securities and sovereign debt instruments

- Market Characteristics: Emerging markets are typically characterized by rapid economic growth rates and ongoing industrialization processes that create unique investment opportunities

- Required Manager Expertise: Successful managers must possess strong fundamental valuation skills combined with deep insight into the specific markets and local conditions in which they invest

- Risk-Return Profile: The primary goal is to achieve higher returns compared to developed markets, though these opportunities come with heightened risks that are unique to emerging market environments

- Political and regulatory instability

- Currency volatility and exchange rate risk

- Lower liquidity and market depth

- Less developed legal and institutional frameworks

Topic 5. Emerging Market Strategy

Module 2. Arbitrage Strategies

Topic 1. Fixed-Income Arbitrage

Topic 2. Convertible Arbitrage

Topic 3. Relative Value Arbitrage

Topic 1. Fixed-Income Arbitrage

- Arbitrage Strategy: Exploits situations where the same asset trades at different prices across markets, two assets with similar cash flows are priced differently, or an asset with a known future price trades at a value that does not reflect its risk-free discounted price

- Fixed-Income Arbitrage - Overview: A long/short approach targeting pricing inefficiencies among fixed-income securities to capture convergence opportunities

- Cross-Border Yield Arbitrage: Exploits temporary divergences between U.S. Treasury yields and hedged yields on Italian government bonds, positioning for eventual yield convergence

- On-the-Run vs. Off-the-Run Strategy: Shorts the more expensive on-the-run 30-year Treasury bond while buying the cheaper off-the-run 29½-year Treasury issued six months earlier; profits as the on-the-run premium fades over time, generating small positive arbitrage returns

Topic 2. Convertible Arbitrage

- Embedded Equity Call Option: A convertible bond contains an embedded equity call option allowing the bondholder to convert the bond into a specified number of common shares when share value exceeds the bond's cash redemption value; bondholder continues receiving coupon payments until conversion is exercised.

- Price Sensitivity Factors: Convertible bond prices are sensitive to three key factors:

- Changes in interest rates

- The issuer's credit risk

- Movements in the issuer's common share price and price volatility

- Three Value Components: The value of a convertible bond comprises:

- Investment value (bond floor value)

- Conversion value (equity component value)

- Option value (value of the conversion right)

- Convertible Bond Arbitrage Strategy: Involves purchasing a convertible bond while simultaneously selling short the underlying stock to profit from bond income and equity volatility; hedge is designed to neutralize equity risk but requires active delta hedging and continuous rebalancing as stock price changes alter the convertible bond's delta.

Topic 2. Convertible Arbitrage

- Arbitrage Profit Sources: Profits are generated through:

- Bond coupon payments

- Interest earned on short sale proceeds

- Main costs include borrowing fees paid to stock lender and dividends owed on borrowed shares

- Monetizing Volatility: Additional returns arise from the nonlinear relationship between stock price and convertible bond price; gains or losses on the short stock position tend to exceed corresponding losses or gains on the convertible bond when prices move, similar to convexity in the bond price-yield relationship.

- Undervaluation Opportunity: Returns can also be generated when the convertible bond is undervalued, particularly when the embedded call option is priced below its fair value.

Topic 2. Convertible Arbitrage

-

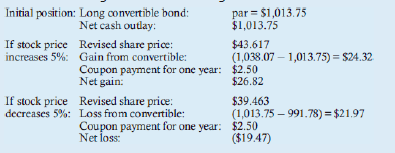

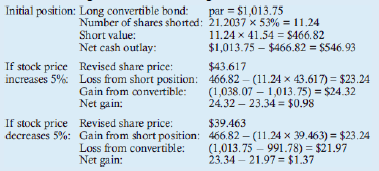

Example: Consider two scenarios that both begin with the purchase of a convertible bond. In the first scenario, the investor goes long the convertible bond but does not hedge the position. In the second scenario, the investor again buys the convertible bond but also establishes an arbitrage trade by shorting a specified quantity of the underlying equity. For both examples, assume the following values:

-

Stock Price: P = $41.54

-

Convertible Delta:

-

Conversion Ratio: R = 21.2037 shares

-

Convertible Price: 101.375% of par = $1,013.75

-

-

Compare the outcomes of the unhedged long position in the convertible bond with those of the hedged convertible arbitrage trade. Specifically, calculate the net gain or loss in each scenario when the underlying stock price increases by 5% and decreases by 5%. Based on those results, explain why the hedged strategy alters the payoff profile relative to the unhedged position.

Topic 2. Convertible Arbitrage

-

Solution:

-

Scenario 1: Unhedged Convertible Arbitrage Trade

-

-

Scenario 2: Hedged Convertible Arbitrage Trade

-

-

-

Summary: In this hedged scenario, the gain is smaller when the stock price rises, but a drop in the stock price also results in a gain rather than the substantial loss seen in the unhedged case. When the stock declines by 5%, the arbitrage position produces a profit of $1.37, compared with a loss of $19.47 in the unhedged long-only strategy.

Practice Questions: Q1

Q1. Which of the following characteristics best defines a convertible arbitrage strategy?

A. Buying undervalued sovereign bonds and shorting corporate bonds.

B. Taking offsetting long and short positions across different yield curves.

C. Buying a convertible bond and shorting the underlying stock to hedge equity exposure.

D. Buying stocks with high dividend yields while shorting stocks with relatively low dividend yields.

Practice Questions: Q1 Answer

Explanation: C is correct.

Convertible arbitrage involves purchasing a convertible bond and shorting the issuer’s stock to hedge equity sensitivity while profiting from income and volatility.

Topic 3. Relative Value Arbitrage

- Relative Value Arbitrage Overview: Seeks to identify pricing inefficiencies across asset classes and attempts to profit from temporary discrepancies between related securities

- Pairs Trading: Long-established strategy targeting correlated stocks within the same industry

- Investor identifies two competing or peer firms that historically exhibited strong price correlation

- When prices temporarily diverge without fundamental news, trader shorts one stock and buys the other

- Expected outcome is spread reversion to prior relationship and convergence

- Statistical Arbitrage: Extension of pairs trading across numerous long and short positions using sophisticated modeling

- Often employs factor models to identify mispricings across large portfolios

- Returns can arise from providing liquidity to institutional investors during large block trades

- Strategy involves buying temporarily mispriced stocks after price declines and shorting related stocks to hedge market risk, holding until normalization

Topic 3. Relative Value Arbitrage

- Index Arbitrage: Trading equity index futures against underlying constituent stocks when mispricing occurs

- Example: Buying S&P 500 Index futures while shorting the 500 constituent stocks

- Computer algorithms optimize subset selection by evaluating transaction costs and other expenses relative to mispricing magnitude

- Firms with existing long positions in constituents gain competitive advantage by sourcing shares internally at lower cost

Practice Questions: Q2

Q2. A pairs trading strategy is best classified as which type of arbitrage?

A. Merger arbitrage.

B. Convertible arbitrage.

C. Fixed-income arbitrage.

D. Relative value arbitrage.

Practice Questions: Q2 Answer

Explanation: D is correct.

Pairs trading is a relative value arbitrage strategy that exploits temporary price divergences between two historically correlated securities.

Module 3. Event-Driven and Distressed Strategies

Topic 1. Event-Driven Strategies

Topic 2. Activist Strategy

Topic 3. Merger Arbitrage

Topic 4. Distressed Securities Strategy

Topic 1. Event-Driven Strategies

-

Overview: Event-driven strategies are designed to capitalize on pricing discrepancies and market inefficiencies created by specific corporate events.

-

Sources: Event-driven investment opportunities can arise from the following categories.

-

1. Strategic Opportunities (Hard Catalysts)

These involve major shifts in a company's structure or ownership.

-

Risk Arbitrage: Profiting from the price gap during mergers and acquisitions.

-

Takeover Targets: Identifying and taking positions in firms likely to be acquired.

-

Spin-offs: Investing in the separation of a division or business unit into an independent company.

-

Stub Trades: Isolating the discount between a holding company’s share price and the actual value of its underlying assets.

-

Strategic Alternatives: Evaluating a firm’s stated options (like a sale or restructuring) and positioning accordingly.

-

Activist Campaigns: Positioning around proxy contests or shareholder-led pressure for change.

-

Topic 1. Event-Driven Strategies

-

Overview: Event-driven strategies are designed to capitalize on pricing discrepancies and market inefficiencies created by specific corporate events.

-

Sources: Event-driven investment opportunities can arise from the following categories.

-

Strategic (Hard Catalysts) Opportunities

-

Financial Opportunities

-

Operational Opportunities

-

Legal and Regulatory Opportunities

-

Technical Opportunities

-

Topic 1. Event-Driven Strategies

-

Strategic Opportunities:

-

Risk arbitrage

-

Evaluating a firm’s strategic alternatives and taking a position

-

Potential spin-offs of divisions or business units

-

Taking positions in likely takeover targets

-

Proxy contests or activist shareholder campaigns

-

Stub trades, which isolate and profit from the discount between a holding company’s share

-

price and the value of its underlying assets

-

-

Financial Opportunities:

-

Anticipating price movements based on credit re-ratings or liquidity events

-

Changes in accounting methods

-

Financial recapitalizations

-

Primary offerings of debt or equity

-

Bankruptcy reorganizations

-

Topic 1. Event-Driven Strategies

-

Operational Opportunities:

-

Synergies from mergers

-

Corporate turnaround or restructuring opportunities

-

Senior management changes

-

-

Legal/Regulatory Opportunities:

-

Taking positions based on litigation outcomes

-

Taking positions based on regulatory changes

-

Taking positions based on anticipated legislation

-

- Technical Opportunities:

-

Broken risk arbitrage situations

-

Secondary offerings of equity or equity-linked notes

-

Topic 2. Activist Strategy

- Strategy Definition: Activist investors take equity or derivative positions in a company and actively seek to influence management or the board of directors to pursue initiatives believed to increase share price and unlock shareholder value

- Proxy Solicitation and Board Pressure: Activists may solicit proxy votes from other shareholders to pressure the board of directors and gain support for proposed changes or to elect activist-aligned board members

- Corporate Governance Changes: Activists advocate for improvements in corporate governance structures, including changes to board composition, executive compensation, transparency, and accountability mechanisms

- Strategic Business Actions: Common activist demands include:

- Spin-offs or divestitures of underperforming business units

- Cost reduction initiatives and operational improvements

- Share repurchase programs to return capital to shareholders

- Increased dividend payments

- Capital Structure Optimization: Activists may push for increased leverage or other capital structure changes intended to enhance returns on equity and overall shareholder value

Topic 3. Merger Arbitrage

- Strategy Goal - Profit from Acquisition Spreads: Merger arbitrage (also known as risk arbitrage) aims to profit from the spread between the acquirer's offer price and the target company's stock price following the announcement of an acquisition, purchase, or merger

- Typical Position Structure - Long Target, Short Acquirer: In share-for-share mergers, the arbitrageur shorts the acquiring firm's stock while simultaneously purchasing the target's stock, unwinding the position at merger completion for profit

- Potential Profit Sources When Deal Closes:

- Arbitrage Spread: Difference between the target firm's stock price at acquisition announcement and the final bid price at closing

- Dividend Income: Dividends received on the target firm's stock during the holding period

- Net Interest Income: Interest earned on proceeds from the short position, less borrowing costs and any dividends owed on the shorted acquirer's stock

- Bid Premium Enhancement: Possibility of an increased bid price, particularly when competing bidders emerge

Topic 3. Merger Arbitrage

- Downside Risks If Deal Fails:

- Target Stock Price Collapse: Target's stock price typically falls back to pre-announcement levels or possibly lower

- Short Position Losses: Acquirer's stock price may rise, creating losses on the short position

- Asymmetric Risk Profile: Losses from a failed deal can far exceed the gains earned when a deal is successfully completed, making risk management critical

- Annualized Expected Return:

-

- Limited Appeal for Long-Only Investors: Mutual funds and other long-only investors often avoid merger arbitrage because the potential upside between the announcement price and acquisition price is small, while there remains uncertainty about whether the deal will successfully close.

-

Hedge Fund Advantage in Merger Arbitrage: Hedge funds participate more actively because they possess specialized expertise in legal, regulatory, and antitrust analysis to assess deal completion probabilities, and they can enhance returns using hedging strategies such as short positions.

Topic 3. Merger Arbitrage

-

Example: Global Semiconductors makes a tender offer to the shareholders of Local Semiconductors at $12 per share. Before the acquisition announcement, Local’s stock was trading at $9 per share, and it immediately rose to $10.50 after the offer. The deal is expected to close in six months, with an estimated 90% probability of completion. Calculate the expected annualized return from entering a merger arbitrage position in Local.

-

Solution: C = 0.90; G = $12 – $10.50 = $1.50; L = $10.50 – $9 = $1.50; P = $10.50; Y = 6 / 12 = 0.50

-

Practice Questions: Q1

Q1. Novelty Healthcare has received a tender offer from a larger competitor. The offer terms specify a price of $30 per share. Before the announcement, Novelty’s stock traded at $25, and it rose to $29 after the offer was made public. Analysts at Primus Fund estimate that the deal has a 75% probability of closing and expect completion within three months. What is the annualized expected return from a merger arbitrage position in Novelty’s stock?

A. −3.45%.

B. −3.33%.

C. 0.25%.

D. 11.25%.

Practice Questions: Q1 Answer

Explanation: A is correct.

- C = probability of success = 0.75

- G = gain if successful = 30-29 = 1

- L = loss of unsuccessful = 29-25 = 4

- P = purchase price = 29

- Y = time to expected close = 3/12 = 0.25 years

Topic 4. Distressed Securities Strategy

- Overview Opportunities

- Overview: Taking speculative positions in securities of firms entering, in, or emerging from bankruptcy, offering a range of return opportunities through discounted acquisitions

- Equity Positions: Investors buy shares in bankrupt companies and hold until emergence from bankruptcy, capitalizing on recovery value

- Non-Investment-Grade Bonds: Purchase attractively priced high-yield bonds that institutional investors and pension funds are prohibited from owning, creating pricing inefficiencies

- Distressed Loan Purchases: Banks sell portions of distressed loans to clean up balance sheets, creating opportunities to acquire debt at discounts

- Trade Claims: Original claim holders often lack expertise or desire to navigate bankruptcy process, creating opportunities to purchase claims at attractive prices

- Core Value Proposition: Acquiring distressed securities or claims at substantial discounts to risk-adjusted values

Topic 4. Distressed Securities Strategy

- Return Opportunities

- Buy-and-Hold Restructuring Strategy: Purchase securities of firms entering restructuring and hold in anticipation of value increase once the firm successfully emerges from the bankruptcy process

- Capital Structure Arbitrage - Senior vs. Junior Mispricing:

- Analyze pricing relationships between senior and junior positions within a firm's capital structure

- Identify mispricings among the issuer's various securities during restructuring

- Execute long-short strategy: purchase undervalued senior securities and short overvalued junior securities

- Exploit expected convergence as senior securities appreciate relative to junior securities during the restructuring process

Topic 4. Distressed Securities Strategy

- Investor Approaches (Active Vs Passive)

- Active Investors: Actively participate in and influence the restructuring process through multiple intervention methods

- Participate on creditor committees to influence restructuring outcomes and protect investor interests

- Supervise the workout process, including both out-of-court restructurings and in-court bankruptcy proceedings

- Engage in legal proceedings when such action could improve their position or recovery prospects

- Passive Investors: Choose not to get involved in restructuring processes and prefer less complex distressed investments

- Focus on distressed securities that require less intensive analysis and monitoring

- Avoid time-consuming involvement in legal proceedings or creditor negotiations

- Prioritize simpler distressed situations with more straightforward investment theses

- Active Investors: Actively participate in and influence the restructuring process through multiple intervention methods

Topic 4. Distressed Securities Strategy

-

Challenges, Risks and Key Considerations:

- Fundamental Uncertainty: Distressed investing involves significant uncertainty due to unstable cash flows, limited liquidity, and complex capital structures that make predicting outcomes difficult

- Valuation Challenges: Valuation is inherently difficult with unreliable recovery estimates, and restructuring or bankruptcy processes often take much longer than initially expected

- Illiquidity Risk: Distressed securities are frequently illiquid, making it difficult to adjust or exit positions without negatively impacting market prices

- Legal and Regulatory Dependencies: Investment outcomes depend heavily on court rulings, creditor negotiations, debtor-in-possession financing arrangements, and potential changes in bankruptcy law

- Legal processes can be unpredictable and extend timelines significantly

- Regulatory changes may alter creditor priorities or recovery expectations

- Competitive and Market Pressures: Competition from other distressed investors, unexpected business deterioration, or issuance of new senior debt can erode expected recovery values and returns

- Specialized Expertise Required: Successful distressed investing demands specialized knowledge in financial analysis, legal processes, and corporate restructuring to navigate the complex landscape effectively

Topic 4. Distressed Securities Strategy

-

Example: Naples Ocean Views (NOV), a real estate holding company, may be forced to file for bankruptcy. The firm has $1 billion of 5% debt maturing in 10 years, which is currently trading at a steep discount of $30 per $100 of face value. Bankruptcy is expected within two years. NOV’s stock is trading at $3 per share. In the event of liquidation, the bonds are estimated to be worth $35 per $100 of face value. Assume an investor follows the distressed strategy of buying one NOV bond with $1,000 face value at $300 and shorting 100 shares of NOV stock at $3. If the firm is liquidated in two years, calculate the gains on the bond position and the equity short position.

-

Solution: Gain on bond position: Receive coupon payments of 5% on $1,000 for two years ($50 per year, total $100), plus $350 in liquidation value, for total inflows of $450. Net gain on the bond = $450 – $300 = $150.

-

Gain on equity short position: Short sale proceeds are $300, and the stock becomes worthless, so the investor does not need to buy back the shares. Net gain on the equity short = $300.

-

Total gain = $150 + $300 = $450

-

Practice Questions: Q2

Q2. Which of the following scenarios best reflects the core risk faced by investors in distressed securities?

A. A restructuring process takes longer than expected.

B. Senior secured creditors receive the lowest recoveries.

C. Bankruptcy guarantees predictable outcomes for all creditors.

D. High trading volume in distressed debt limits position building.

Practice Questions: Q2 Answer

Explanation: A is correct.

Distressed investing carries significant timing risk, because prolonged restructuring or bankruptcy proceedings can erode expected returns.