Book 5. Risk and Investment Management

FRM Part 2

IM 10. The Rise And Risks of Private Credit

Presented by: Sudhanshu

Module 1. Private Credit Characteristics

Module 2. Private Credit Risks

Module 1. Private Credit Characteristics

Topic 1. Characteristics of Private Credit

Topic 2. Private Credit Investors and Borrowers

Topic 3. Private Credit vs. Other Types of Loans

Topic 4. Private Credit Growth

Topic 5. Private Credit Returns

Topic 1. Characteristics of Private Credit

- Private Credit Definition and Structure: Nonbank corporate credit from bilateral agreements, excluding public securities and commercial banks; primarily involves asset managers obtaining funding from institutional investors through closed-end fund structures to lend to middle-market companies

- Target Market Niche: Services mid-sized companies with annual revenues between $100 million and $1 billion

- Borrowing requirements exceed what single commercial banks can reasonably provide

- Companies not large enough to raise funds through public offerings

- Loan Characteristics and Terms: Loans established directly between asset managers (lenders) and borrowers

- Total costs (interest payments) typically higher than traditional bank loans

- Greater customization of lending terms (e.g., deferred interest payments)

- Extensive use of protective covenants (limits on dividend distributions, share buybacks, asset sales)

- Relationship and Flexibility Advantages: Superior relationship management compared to bank loans and public debt

- Provides greater flexibility when working with delinquent loans

- Results in increased repayments and reduced defaults

-

Typical Investors

- Institutional Investors with Long Horizons: Pension funds, insurance companies, sovereign wealth funds, and family offices are primary investors in private credit

- Common Structures:

- Closed-end fund structures (similar to private equity)

- Business development companies (BDCs)

- Collateralized loan obligations (CLOs)

- Typical Borrowers

- Company Profile: Small and mid-sized companies, commonly in information technology and healthcare sectors

- Loan Characteristics:

- Floating-rate basis with more collateral requirements and covenants than traditional bank loans

- Tailored loan terms suited to borrower's specific business operations

- Credit Risk Profile: Generally considered higher risk than high-yield bond or leveraged-loan issuers; tend to have weak earnings and/or high leverage, often not qualifying for traditional bank financing

- Risk Mitigants: Private equity backing and strong lender relationships reduce liquidity and solvency risks despite weaker credit profiles

Topic 2. Private Credit Investors and Borrowers

Practice Questions: Q1

Q1. To minimize liquidity risk, which of the following investment structures would most likely be utilized as an intermediary between borrowers and end investors in a private credit structure?

A. Closed-end fund.

B. Open-ended fund.

C. Collateralized loan obligation (CLO).

D. Business development company (BDC).

Practice Questions: Q1 Answer

Explanation: A is correct.

Closed-end funds comprise over 80% of the total private credit market. They have a capital call structure and limited lifecycle that are comparable to private equity funds. The limitations on redemptions under the closed-end structure greatly assist in reducing liquidity risk. The other structures are far less common (e.g., about 5% for CLOs and about 14% for BDCs).

-

Alternatives to Private Credit

-

Traditional Bank Loans: Conventional lending directly from banks to borrowers as an alternative financing source

- Public Debt Issuance: Companies can raise capital by issuing bonds or other debt securities in public markets

- Broadly Syndicated Loans: Multiple lenders collectively provide financing to a single borrower when the loan amount or risk exposure is too large for one lender

- Used to distribute risk across multiple institutions

- Allows for larger total loan amounts than single-lender arrangements

- Leveraged Loans: A specific type of broadly syndicated loan for highly leveraged corporate entities

- Typically rated noninvestment grade (below BBB-/Baa3)

- Carries higher interest rates to compensate for increased credit risk

- Borrower has significant existing debt relative to equity or cash flow

-

Topic 3. Private Credit vs. Other Types of Loans

- Post-Crisis Expansion: Private credit experienced tremendous growth following the 2007–2009 financial crisis, driven by extended low interest rates making it an increasingly attractive alternative financing source for borrowers

- Regulatory Environment Impact:

- Stricter regulatory requirements for financial institutions created opportunities for private credit

- Insurance companies entered the private credit lending market due to less onerous capital charges and risk requirements compared to commercial banks

- Further regulatory increases could accelerate movement toward private credit

- Market Size and Composition:

- Reached approximately $2.1 trillion in loans and undeployed capital as of 2023

- Comparable in size to the global high-yield bond market

- Primarily managed in North America despite noticeable growth in Europe and Asia

Topic 4. Private Credit Growth

- Expanding Borrower Base:

- Original focus on mid-sized borrowers has expanded to larger corporate entities

- Companies that traditionally used syndicated loans or public bond issuances now utilize private credit

- Shift driven by tailored borrowing structures, reduced disclosure requirements, and lower costs versus public issuances

- Regional Growth Rates and Penetration:

- United States and Asia: approximately 20% annual growth over past five years

- Europe: 17% average annual growth over the same period

- Market penetration (as of June 2023): 7% of total corporate credit in US, 1.6% in Europe, 0.2% in Asia

- Private Equity Connection: Private credit growth mirrors private equity expansion, with substantial private credit lending involving borrowers backed by private equity firms

Topic 4. Private Credit Growth

- Recent Performance (Since 2020):

- Private equity has significantly outperformed private credit

- Private credit performance similar to natural resources

- Private credit has somewhat better performance than real estate

- Private credit has significantly outperformed S&P 500 and venture capital

- Post-Financial Crisis Period (2008-2020):

- Private credit outperformed both private equity and real estate for approximately 10 years

- Private equity and real estate returns were similar during this period

- Significant inflection point around 2020 when private equity returns surged dramatically ahead of private credit

- Natural Resources Comparison:

- Private credit underperformed natural resources from approximately 2008 to 2016

- Since 2016, private credit and natural resources have delivered similar returns

Topic 5. Private Credit Returns

Practice Questions: Q2

Q2. In recent years, which of the following asset classes has outperformed private credit?

A. Real estate.

B. Private equity.

C. Venture capital.

D. Natural resources.

Practice Questions: Q2 Answer

Explanation: B is correct.

Regarding returns in recent years (since 2020), private equity has significantly outperformed private credit, while private credit has had similar performance as natural resources and somewhat better performance than real estate. Private credit has significantly outperformed the S&P 500 and venture capital during this time period.

Module 2. Private Credit Risks

Topic 1. Risks to Financial Stability

Topic 2. Credit Risks

Topic 3. Liquidity Risks

Topic 4. Leverage Risks

Topic 5. Valuation Risks

Topic 6. Interconnectedness Risks

Topic 7. Underwriting Standards

Topic 8. Policies for Mitigating Private Credit Risks

Topic 9. Credit Risks Mitigation

Topic 10. Liquidity Risks Mitigation

Topic 11. Leverage Risks Mitigation

Topic 12. Valuation Risks Mitigation

Topic 13. Interconnectedness Risks Mitigation

Topic 14. Conduct Risks Mitigation

Topic 1. Risks to Financial Stability

-

Private Credit: Shift and Transparency Concerns

- Credit Market Shift: Credit provision has moved from safe, regulated entities (banks with heavy regulation, public bonds with extensive disclosures) to less transparent and less regulated private credit firms with nonrated, nontraded loans lacking standardized terms

- Transparency Challenges: Lack of transparency makes timely risk identification difficult; insufficient information available for thorough financial stability analysis; widespread risks with potential major systemic impacts remain poorly understood

- Untested Resilience: Rapid rise of private credit has not experienced a serious market correction, so long-term stability remains unvetted

- Current Risk Profile and Emerging Concerns

- Moderate Current Risks: Asset-liability duration matching appears reasonable with relatively low leverage; liquidity and interconnectedness risks seem low at present

- Underwriting Standards Risk: Competitive pressure for business may lead to reduced underwriting standards, increased expected losses, and potentially ineffective risk management tools

- Market Terms Deterioration: Increased private credit supply may result in reduced risk premiums and less onerous covenants as firms compete to generate lending revenues

Topic 1. Risks to Financial Stability

-

Potential Systemic Risks

- Credit Risk from Rate Sensitivity:

- Borrowers tend to be small and highly leveraged

- Private credit loans are mainly floating-rate; rate increases hurt borrowers and may trigger widespread defaults, reducing lender profitability

- Investor Concentration Risk: Significant institutional holders (insurance companies, pension funds) lack knowledge and transparency about underlying assets; vulnerable to large losses in sudden economic downturns

- Liquidity Risk: As private credit funds expand to wider public investor base, less liquid funds face redemption risk when mass groups attempt simultaneous withdrawals

- Interconnectedness Risk:

- Complex leverage labyrinth involving multiple participants (borrowers, funds, investors)

- Large capital calls in stressed markets could create domino effects and economy-wide funding reduction

- Valuation Risk:

- Insufficient price discovery mechanisms with minimal regulatory monitoring

- Lack of borrower transparency prevents objective exposure determination

- Fund managers may defer unrealized losses, creating concentrated realization events that trigger default waves

- Financial Stability Risk: Multiple financial sector groups hold private credit (pension funds, private equity, insurance companies); lack of information prevents regulators from examining spillover effects

- Conduct Risk: Unsophisticated investors may not properly understand private credit risks or fund withdrawal constraints before investing

- Credit Risk from Rate Sensitivity:

Topic 2. Credit Risks

-

Credit risk in private credit is characterized by below factors:

-

Interest Rate Sensitivity: Private credit borrowers are highly sensitive to rising interest rates since virtually all loans are floating rate

- Borrowers often receive temporary relief through payment-in-kind (PIK) arrangements where unpaid interest is added to outstanding debt

- Lenders face default risk if borrowers continue generating insufficient cash flow for interest payments and debt reduction

- Historical Loss Performance: Private credit losses have historically been lower than high-yield bonds and comparable to leveraged loans

- Private equity firm backing has significantly reduced default rates

- Collateral requirements for most private credit loans have minimized credit losses

- Cyclical Behavior Questions: The cyclical nature of private credit remains somewhat unclear with mixed evidence

- Counter-cyclical evidence: Private credit funding continued during stressed markets when traditional funding sources dried up (e.g., March 2020)

- Pro-cyclical evidence: Amount of private credit funding available shows positive correlation with equity market returns

- Bank lending relationship: Positive correlation exists between stricter bank lending standards and reduction in new private credit lending

-

Practice Questions: Q1

Q1. Historically speaking, which of the following asset classes has experienced the highest level of losses?

A. Leveraged loans.

B. High-yield bonds.

C. Private credit loans.

D. Broadly syndicated loans.

Practice Questions: Q1 Answer

Explanation: B is correct.

Private credit losses have historically been lower than those for high-yield bonds, and private credit losses are similar to those for leveraged loans (leveraged loans are below investment grade). The backing of private equity firms has certainly reduced defaults. Additionally, the fact that most private credit loans require collateral has also reduced the amount of credit losses. In general, syndicated loans have a relatively deep secondary trading market and are investment grade, so their losses are likely the lowest of all four answer choices.

Topic 3. Liquidity Risks

-

Liquidity risk and its management in private credit has several dynamic components, as listed below.

- Cash Flow Mismatch Mitigation

- Private credit funds face potential cash flow mismatches due to illiquid underlying assets (e.g., private corporate loans)

- Impose long-term lockups to reduce cash outflows to investors

- Lending activities increase cash outflows and liquidity risks

- Semiliquid evergreen fund structures (continuously accepting capital and making new investments) further increase liquidity risk

- Structure-Specific Liquidity Profiles

- CLOs and Closed-End Funds: Generally do not permit fund withdrawals, greatly mitigating liquidity risk

- Semiliquid Funds: Allow investor redemptions at specified times only, attracting broader investor base including retail investors but creating liquidity challenges

Topic 3. Liquidity Risks

- Redemption Restrictions and Controls

- Gates: Maximum withdrawal amounts to limit redemption pressure

- Suspensions: Deferral of payment following redemption requests

- Limited redemption periods help control liquidity risk

- Trade-off: More frequent redemption periods attract individual investors but increase liquidity risk

- Credit Line Drawdown Risk

- Sudden, unexpected draws on credit lines by multiple borrowers simultaneously create additional cash flow needs

- May necessitate investor capital calls, effectively shifting liquidity risk from the fund to investors

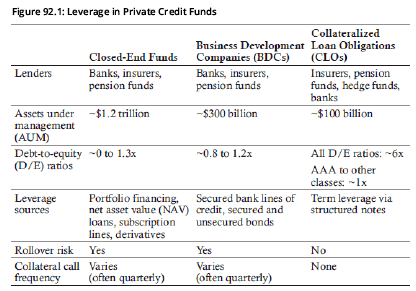

Topic 4. Leverage Risks

- Multi-Layered Leverage System: Leverage exists at multiple levels beyond the fund itself—including investors, funds, and borrowers—making it nearly impossible to determine the collective impact on overall financial stability due to lack of transparency

- Investor-Level Leverage Risks:

- Pension funds and insurance companies commonly employ leverage when investing in private credit

- Exposes these institutions to potential credit downgrades and defaults

- Their size can create negative spillover effects on other market participants when satisfying margin and collateral calls during stressed markets

- Fund-Level Leverage Mechanisms:

- Achieved through special purpose vehicles (SPVs) and complex structures

- Collateralized fund obligations (CFOs) move limited partner interests to SPVs to reduce cash outflows and accommodate more investors

- Borrower-Level Leverage:

- Private credit borrowers are often highly leveraged through multiple channels

- Borrow from both private credit funds and the private equity firms backing them

Topic 4. Leverage Risks

- Systemic Risk Concerns:

- Leverage can mask reporting deficiencies, creating risk of large losses during funding stress

- Borrower defaults cascade to fund losses and investor losses

- Capital call requirements may require substantial funding, potentially causing system-wide liquidity crisis as all lenders simultaneously reduce lending activities

- Main Leverage Structures: Private credit funds utilize three primary forms to magnify investor returns:

- Closed-end funds

- Limited data available on leverage utilization;

- Most closed-end private credit funds do not utilize leverage

- Business development companies (BDCs):

- More diversified debt sources through issuance of unsecured debt;

- subject to regulatory leverage caps despite being regulated entities;

- Leverage levels have gradually increased over time

- Middle-market collateralized loan obligations (CLOs):

- Structured with multiple tranches allowing different investor types to select risk levels matching their risk tolerance

- Investors include insurance companies, pension funds, hedge funds, banks

- Closed-end funds

Topic 4. Leverage Risks

- Market Stress Vulnerabilities:

- Minimum loan-to-value ratio requirements can trigger onerous collateral calls when asset values decline during stressed markets

- Revolving credit lines create risk of simultaneous draws by multiple borrowers, requiring substantial additional funding capacity

Topic 5. Valuation Risks

-

Limited Valuation Usefulness

-

Core Issues: Private credit valuations have limited utility due to few or no comparable transactions, infrequent valuations, and absence of secondary markets to corroborate valuations

- Liquidity Crisis Risk: In economic downturns, stale valuations may trigger mass investor withdrawals from private credit funds, though redemption limitations effectively mitigate this liquidity risk

-

-

Valuation Methodology Problems

-

Illiquidity Challenges: Long-term loans are illiquid and specifically designed for individual parties, making it difficult to find comparable transactions for accurate valuation

- Subjective Assessments: Market estimates and external valuators provide subjective assessments influenced by biases

- Lack of Standards: Neither accounting standards nor regulations mandate consistent valuation methodologies, preventing meaningful comparisons across funds

-

Topic 5. Valuation Risks

-

Price Sensitivity and Discounts

-

Lower Shock Sensitivity: Private credit asset prices are less sensitive to market shocks compared to high-yield bonds and leveraged loans

- Offsetting Valuation Discounts: Additional valuation discounts offset the lower price sensitivity, with discounts increasing during economic downturns

- Stale Pricing: Compared to public debt, private credit loan value changes are lower and less responsive, causing prices and net asset value to differ significantly for several quarters

-

-

Advantages of Stale Valuations

-

Minimized Runoff Risk: While stale valuations could allow astute investors to withdraw before write-downs, redemption restrictions substantially minimize this risk

- Reduced Volatility: Infrequent valuations may reduce market volatility, as estimation error and unreliable data make frequent valuations potentially counterproductive

- Long-Term Focus: Less frequent valuations prevent excessive focus on short-term results, preserving the longer-term investment benefits of private credit

-

Topic 5. Valuation Risks

-

Disadvantages of Stale Valuations

-

Impaired Risk Assessment: Infrequent valuations prevent investors from accurately assessing risks and making effective investment decisions

- Inflated Return Perception: Stale valuations may suggest higher returns than actual current-period returns, misleading investors while benefiting managers attracting new capital

- Fee Overpayment: Overstated asset values can result in overpayment of manager fees based on inflated asset bases

- Understated Losses: Deferred losses lead to understatement of actual losses, causing investors to inaccurately assess their true investment risk exposure

-

Topic 6. Interconnected Risks

-

Interconnections among Market Participants

- Private Equity-Private Credit Linkage: Many private credit managers are also private equity managers; numerous borrowing firms are backed or guaranteed by private equity sponsors, significantly reducing credit risk but creating potential contagion if weaknesses emerge in either sector

- Conflict of Interest Risk: Numerous connections among managers increase the risk of conflicts of interest across the private credit ecosystem

-

Bank and Institutional Investor Exposure

- Limited Bank Exposure: Banks have minimal exposure to private credit firm lending (under 1% of total assets), further mitigated by secured lending basis

- Pension and Insurance Investment: Pension funds and insurance companies are primary investors in private credit, with exposures limited to approximately 3% of assets under management

-

Private-Equity Influenced Life Insurance Concerns

-

Cash Flow Utilization: PE-influenced insurers provide PE firms with reliable premium cash flows that can be invested in illiquid assets established by the PE firms themselves

- Solvency Concerns:

- Hold greater illiquid asset holdings compared to other life insurers

- Weaker-than-average solvency capital ratios despite higher illiquid assets

- Regulatory capital could be quickly wiped out by sudden increase in defaults

- Risk amplified by inherent leverage in underlying illiquid assets (e.g., ABSs)

-

Topic 6. Interconnected Risks

-

Liquidity Risk for Institutional Investors

- Pension Fund Liquidity Mismatch:

- Hold increasing amounts of illiquid assets (private equity and private credit) while extensively using derivatives

- Face heightened liquidity risk from potential margin and collateral calls on derivatives positions given illiquid asset base

- Capital Call Risk: Private credit funds may impose sudden capital calls on investors; pension funds and insurance companies may have uncalled capital commitments exceeding current private credit investments

- Defined-Contribution Plan Timing Conflict: Private credit assets in DC plans create mismatch between beneficiaries' short-term switching options and long-term nature of private credit investments, generating additional liquidity risk

- Pension Fund Liquidity Mismatch:

Practice Questions: Q2

Q2. In the context of vulnerabilities and potential risks to financial stability in corporate private credit, which of the following risks is currently of greatest concern?

A. Credit risk.

B. Conduct risk.

C. Liquidity risk.

D. Interconnectedness risk.

Practice Questions: Q2 Answer

Explanation: D is correct.

Interconnectedness risk is also related to leverage risk due to the existence of multiple layers of leverage. This risk exists because the private equity and private credit industries are closely intertwined. For example, many borrowing firms in private credit loans have a private equity sponsor. Although this mitigates credit risk, it does exacerbate interconnectedness risk. The close connection between private credit and private equity suggests that vulnerabilities in one could easily spill over to the other.

Topic 7. Underwriting Standards

- Increased Competition: Rapid growth of private credit has intensified competition among banks, public bond markets, and private lenders for larger corporate borrowers

- Collaborative Lending: Banks and other lenders increasingly partner with private credit firms to provide larger loan facilities

- Deteriorating Lending Standards:

- Diminished underwriting standards with loans priced too low relative to actual risk levels

- Less strict loan covenants imposed by private credit lenders

- Pricing not commensurate with underlying credit risk

- Systemic Risk Exposure: Banks and other lenders face potential for significant losses in the event of an adverse economic downturn with elevated default rates

Topic 8. Policies for Mitigating Private Credit Risks

- Need for Stronger Controls: The massive growth in private credit threatens financial stability, necessitating stronger regulatory controls and greater oversight globally

- Expanded Regulatory Framework:

- United States and European Union have expanded regulations to address systemic risks

- Asian jurisdictions have also strengthened oversight

- Regulatory focus areas include conflicts of interest, conduct standards, valuation practices, and disclosure requirements

- Cross-Border Coordination Approach: Most effective risk management requires enhanced regulations and supervisory activities on both cross-sectoral and cross-border bases, with authorities from different jurisdictions collaborating to understand risks, impacts, and potential collateral effects on other asset classes and systemic institutions

- Six Key Policy Risk Areas: Policy recommendations should address:

- Credit risk,

- Liquidity risk,

- Leverage risk,

- Valuation risk,

- Interconnectedness risk, and

- Conduct risk

Topic 9. Credit Risks Mitigation

- Regulatory Gap: Insurance companies and pension funds face no formal requirements to monitor the creditworthiness of underlying loan assets

- Reliance on External Assessment: Substantial dependence on internal valuations and external credit rating agencies, which may provide limited confidence in risk assessment

- Enhanced Monitoring Imperative: Funds with significant private credit exposure should implement rigorous bank-like processes to monitor performance in:

- Structured products

- Direct lending portfolios

- Critical Scrutiny Areas: Underwriting policies, procedures, and credit risks require careful examination due to potential for significant negative systemic impacts across the financial system

Topic 10. Liquidity Risks Mitigation

- Current Concerns: Open-ended fund structures and generous redemption policies create liquidity mismatch risks, particularly for funds holding illiquid assets; risk amplified when unsophisticated investors attempt mass withdrawals during stressed economic conditions

- Structural Remedies:

- Allow only closed-end fund structures to eliminate redemption pressure

- Reduce redemption frequency to limit withdrawal timing

- Mandate longer notice periods for redemptions and extended settlement timeframes

- Operational Remedies: Implement stricter rules requiring liquidity management techniques and comprehensive stress testing for funds with substantial liquidity mismatches

- Investor Protection: Mandate thorough, understandable disclosures regarding investment risks and redemption restrictions to better educate investors about liquidity constraints

Topic 11. Leverage Risks Mitigation

-

Information Gaps and Reporting Issues

- Insufficient data available to accurately determine leverage levels employed in private credit markets

- Reported information often omits or obscures interconnected leverage sources such as special purpose vehicles (SPVs) and feeder/master fund structures

- Data omissions and reporting inconsistencies across countries and sectors prevent comprehensive oversight of total leverage

- Liquidity Management Requirements: Private credit firms should demonstrate strong liquidity management processes to their lending banks, including:

- Stress testing for constrained funding sources

- Stress testing for write-downs on leveraged assets

- Stress testing for large and abrupt credit drawdowns by borrowers

- Regulatory Solutions

- Implement enhanced reporting requirements both domestically and internationally

- Strengthen cooperation between cross-border regulators to address data deficiencies

- Consider imposing leverage caps when levels become excessive and pose systemic risk

Topic 12. Valuation Risks Mitigation

- Current Regulatory Gap: Regulations do not mandate specific asset valuation methods; institutional investors determine their own valuations, leading to significant valuation differences for the same asset depending on methodology used

- Proposed Regulatory Solutions:

- Greater regulatory oversight of valuation methods used by financial entities

- Mandatory external valuations when asset values are significant or prone to error

- Regular audits of valuations to identify deficiencies in methods and internal controls for prompt correction

- Critical Risk Area: Key valuation risk involves asset write-downs of illiquid and semiliquid assets; losses must be accurately determined and recognized in the appropriate reporting period

Topic 13. Interconnected Risks Mitigation

- Regulatory Arbitrage in Private Credit:

- More private credit risk is taken in countries and sectors with less strict regulations, as market participants seek favorable regulatory treatment

- Insurance companies and pension funds hold substantial private credit holdings, potentially driven by regulatory arbitrage opportunities

- Interconnections between these institutions create significant systemic risk concerns that warrant regulatory attention

- Cross-Border Regulatory Cooperation:

- Lack of data on interconnected risks requires international regulatory cooperation to ensure proper oversight, particularly for concentrated risks

- Regulators across different sectors must collaborate locally to identify additional information needs, understand interconnected risks, and mitigate contagion risks

- Harmonization Imperative:

- Regulatory arbitrage occurs both domestically and internationally as firms seek least onerous regulations

- Concentrated risks necessitate harmonization of risk assessment processes across sectors and borders to reduce or eliminate regulatory arbitrage opportunities

Topic 14. Conduct Risks Mitigation

- Investor Protection Concerns: Greater numbers of unsophisticated investors in private credit create heightened conduct risks, particularly where funds are involved on both sides of transactions, necessitating measures to avoid conflicts of interest

- Valuation and Pricing Risks:

- Private transactions may be unfair to one party due to lack of market pricing controls

- Frequent redemption options can incentivize managers to manipulate valuations to discourage withdrawals

- Managers may make redemptions conditional on reinvesting funds in other manager-controlled investments

- Supervisory Responsibilities:

- Determine existing conduct risks and recommend increased disclosure when conflicts of interest arise

- Prioritize investors' best interests by ensuring fair sales practices and adequate assessment of investment suitability

- Implement controls to ensure retail investors understand credit and liquidity risks and redemption restrictions

Practice Questions: Q3

Q3. Which of the following statements regarding policy recommendations on private credit risks is most accurate?

A. The provision of more frequent redemptions to investors within private credit fund investments gives rise to potential conduct risks.

B. Given that private credit risks are largely mitigated, authorities need to be careful not to take an overly regulatory approach that would limit the growth of this emerging asset class.

C. The existence of regulatory arbitrage across borders and sectors has helped in mitigating excessive concentration of private credit risk in certain jurisdictions and sectors.

D. To address private credit asset valuation risks on a cost-effective basis, regulators should consider mandating either independent external valuations or strengthening managers’ internal governance mechanisms on valuation procedures.

Practice Questions: Q3 Answer

Explanation: A is correct.

Allowing for more frequent redemptions by investors could cause managers to manipulate valuations to discourage redemptions or to make the redemptions conditional upon investing the redeemed funds in other investments controlled by the manager, thereby potentially increasing conduct risk.

IM 10. The Rise and Risks of Private Credit

By Prateek Yadav